Campaign 3: Break the Debt Chain

The Complete Financial Sovereignty Guide

A Sovereignty Module of the Practitioner Community

Preamble

Money is the second-greatest chain after food. Most humans spend 40+ years exchanging irreplaceable time for depreciating currency, then transfer the majority of that currency to banks through interest payments they never fully understand. This campaign gives any individual the mathematical proof of how the system extracts wealth, the exact protocols to escape it, and the knowledge to build a sovereign financial foundation that no institution can seize, inflate, or deny.

Every number in this document is arithmetic. Every claim is verifiable with a calculator. No belief required. Only math.

Part I: How Money Actually Works (What They Never Teach)

Chapter 1: The Creation of Money as Debt

The most important fact about modern money that is deliberately excluded from public education: money is created as debt. Not backed by debt. Not related to debt. Created AS debt, simultaneously, in the same transaction.

The Fractional Reserve Mechanism

When you take a "loan" from a bank, the bank does not lend you money from its vault or from other depositors' savings. The bank creates new money at the moment of lending by typing numbers into your account. This is not conspiracy theory. It is published by central banks themselves:

"Whenever a bank makes a loan, it simultaneously creates a matching deposit in the borrower's bank account, thereby creating new money." (Bank of England Quarterly Bulletin, Q1 2014, "Money Creation in the Modern Economy")

| Step | What Happens | Result |

|---|---|---|

| 1 | You apply for a $200,000 mortgage | Bank evaluates your ability to repay |

| 2 | Bank approves loan | Bank types $200,000 into your account (new money, created from nothing) |

| 3 | You buy a house | $200,000 transfers to seller |

| 4 | You repay over 30 years | You pay back $200,000 PLUS approximately $185,000 in interest (at 5%) |

| 5 | Total repayment | $385,000 for a $200,000 creation |

| 6 | The $185,000 interest | Was never created. Must come from OTHER people's loan-money circulating in the economy. |

The Mathematical Impossibility

This is the core insight: banks create the principal but NOT the interest. If all money in circulation is created as loans, and all loans require repayment of principal PLUS interest, then there is always more debt in the system than money to repay it. This is not a flaw. It is the design. It guarantees:

- Perpetual scarcity (there is never enough money for everyone to be debt-free simultaneously)

- Perpetual competition (humans must compete for the insufficient money supply)

- Perpetual wealth transfer (interest flows from borrowers to lenders, concentrating wealth)

- Perpetual growth requirement (new loans must be created to service existing interest, requiring economic "growth" forever)

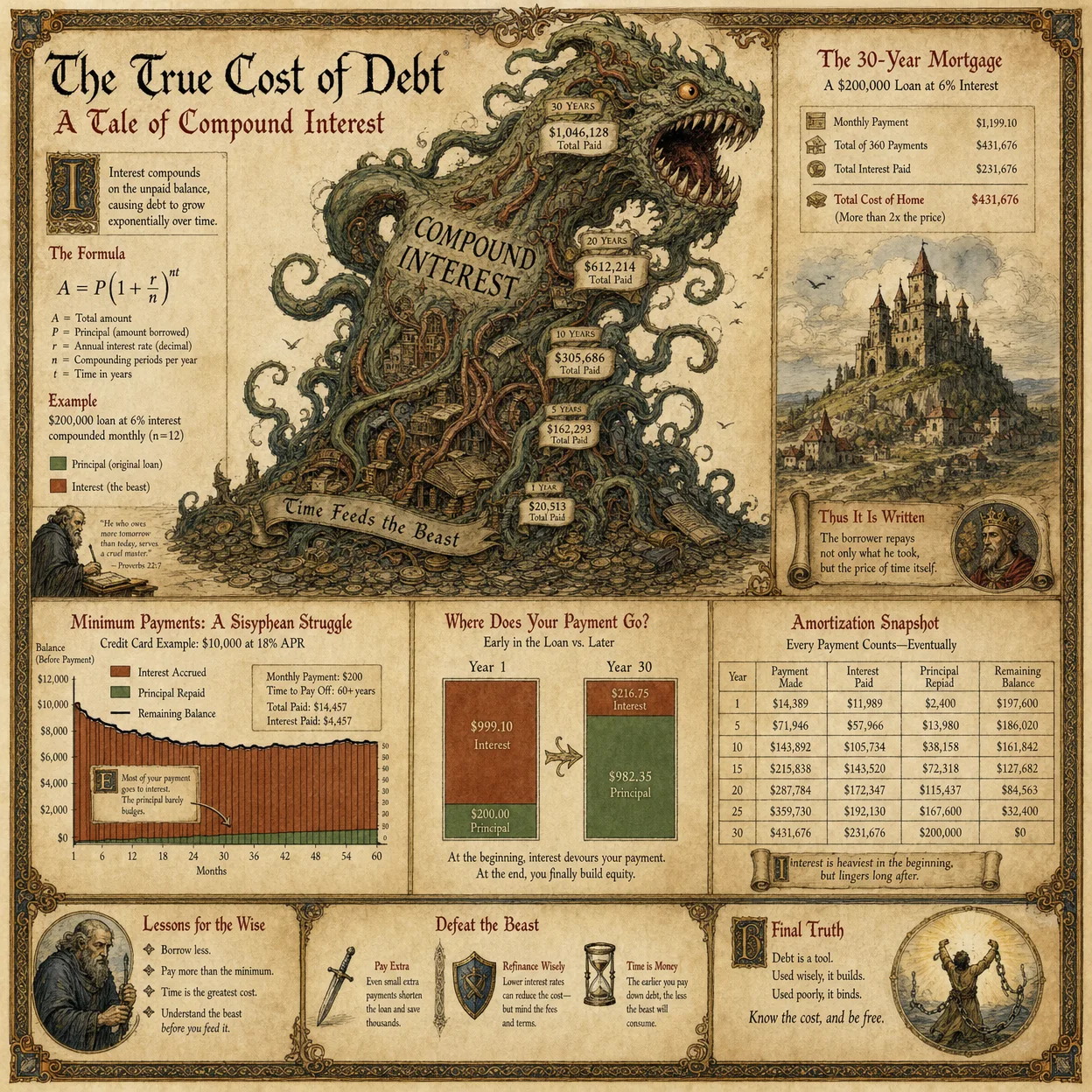

Chapter 2: The Compound Interest Trap

Compound interest is the mechanism by which small debts become permanent chains. Albert Einstein is widely attributed the quote: "Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn't, pays it." Whether Einstein said it or not, the mathematics are absolute.

The Rule of 72

Divide 72 by the interest rate to find how many years it takes for a debt (or investment) to double.

| Interest Rate | Years to Double | Example |

|---|---|---|

| 3% | 24 years | $10,000 becomes $20,000 in 24 years |

| 5% | 14.4 years | $10,000 becomes $20,000 in 14.4 years |

| 7% | 10.3 years | $10,000 becomes $20,000 in 10.3 years |

| 12% | 6 years | $10,000 credit card debt becomes $20,000 in 6 years |

| 18% | 4 years | $10,000 credit card debt becomes $20,000 in 4 years |

| 24% | 3 years | $10,000 store credit becomes $20,000 in 3 years |

The True Cost of a 30-Year Mortgage

| Loan Amount | Interest Rate | Monthly Payment | Total Paid Over 30 Years | Total Interest Paid | Interest as % of Principal |

|---|---|---|---|---|---|

| $200,000 | 4% | $955 | $343,739 | $143,739 | 72% |

| $200,000 | 5% | $1,074 | $386,512 | $186,512 | 93% |

| $200,000 | 6% | $1,199 | $431,676 | $231,676 | 116% |

| $200,000 | 7% | $1,331 | $479,017 | $279,017 | 140% |

| $300,000 | 7% | $1,996 | $718,527 | $418,527 | 140% |

At 7% interest, you pay 140% of the home's value in interest alone. You buy the house twice and give one to the bank. This is the chain.

Chapter 3: Inflation (The Hidden Tax)

Inflation is not "prices going up." Inflation is the purchasing power of your money going down because more money is being created (as debt) faster than goods and services are being produced.

Purchasing Power of $1 Over Time (US Dollar)

| Year | Purchasing Power of 1913 Dollar | What Happened |

|---|---|---|

| 1913 | $1.00 | Federal Reserve created |

| 1933 | $0.52 | Gold confiscation (Executive Order 6102) |

| 1971 | $0.18 | Nixon ends gold convertibility |

| 1980 | $0.08 | Stagflation era |

| 2000 | $0.04 | Dot-com era |

| 2020 | $0.02 | Pre-pandemic |

| 2024 | $0.015 | Post-pandemic money creation |

The dollar has lost 98.5% of its purchasing power since the Federal Reserve was created in 1913. This is not a failure of the system. It is the system working as designed: a slow, invisible transfer of wealth from savers to money-creators.

Who Benefits from Inflation:

- Those closest to new money creation (banks, government, large corporations who borrow first)

- Asset holders (real estate, stocks rise nominally with inflation)

- Debtors with fixed-rate loans (debt becomes easier to repay in devalued dollars)

Who Is Harmed by Inflation:

- Savers (purchasing power destroyed)

- Workers on fixed wages (real wages decline)

- Retirees on fixed income (savings buy less each year)

- Anyone holding cash (guaranteed loss of value)

Chapter 4: The Federal Reserve (Neither Federal Nor a Reserve)

The Federal Reserve System was created by the Federal Reserve Act of 1913. It is not a government agency. It is a consortium of private banks with a government-granted monopoly on money creation.

| Common Belief | Documented Reality |

|---|---|

| "The Fed is a government institution" | The Fed is a private corporation with shareholders (member banks). It has never been audited by the government. (Bloomberg FOIA lawsuit, 2011) |

| "The Fed protects the economy" | Since 1913: Great Depression (1929), stagflation (1970s), S&L crisis (1980s), dot-com crash (2000), housing crash (2008), COVID response ($4.5 trillion created 2020-2021) |

| "The Fed is accountable to the public" | Fed Chair is appointed, not elected. Fed meetings are private. Full audit has never been conducted. Ron Paul's "Audit the Fed" bill passed House but blocked in Senate repeatedly. |

| "The Fed controls inflation" | The Fed IS inflation. Every dollar created (as debt) dilutes existing dollars. |

Part II: Breaking Free (The Escape Protocols)

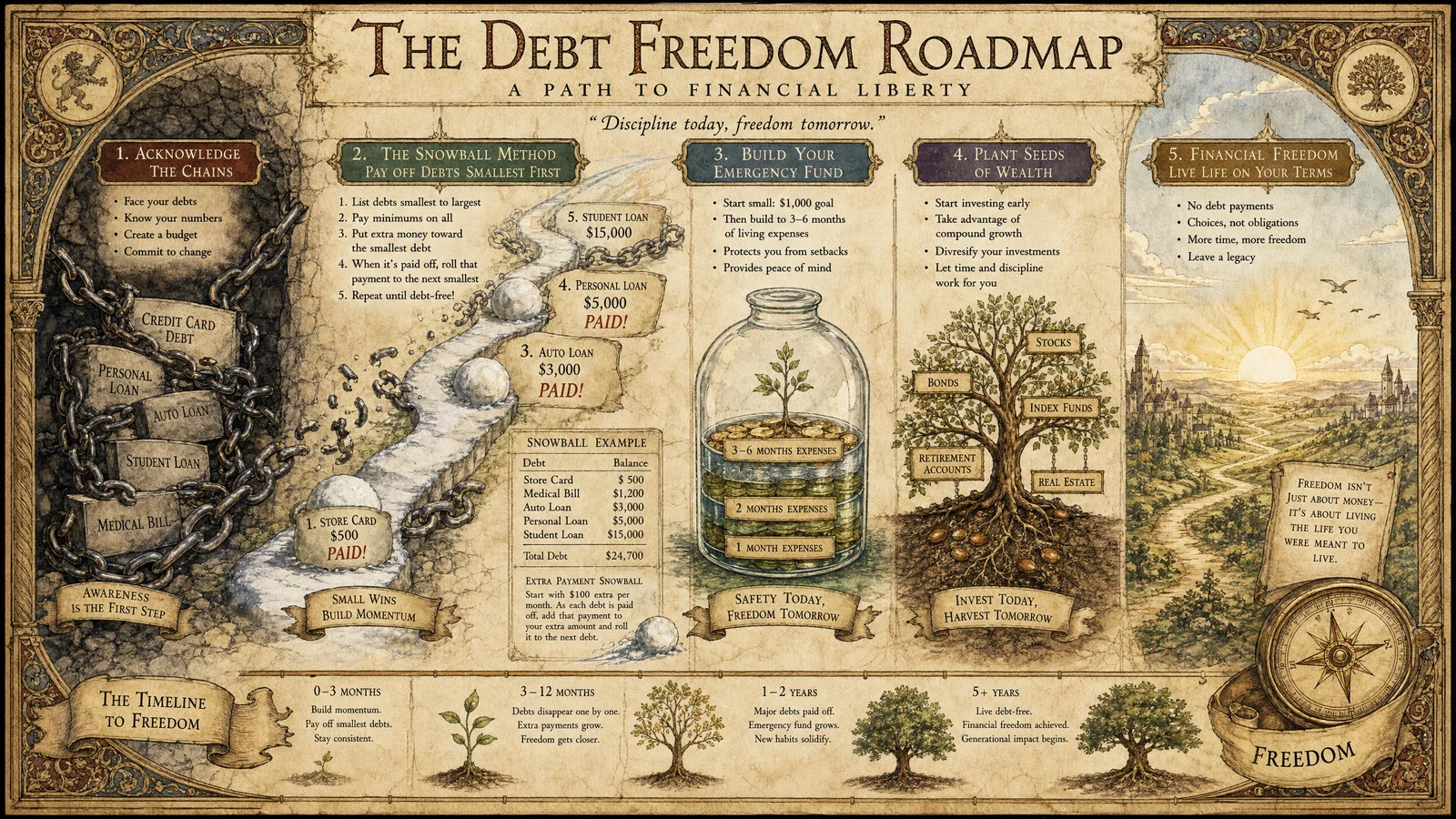

Chapter 5: The Debt Elimination Sequence

Debt elimination is not about willpower or sacrifice. It is about mathematics and sequence. The two proven methods:

Method 1: The Avalanche (Mathematically Optimal)

Pay minimum on all debts. Direct all extra money to the highest-interest debt first. When that is eliminated, redirect its payment to the next-highest-interest debt. Repeat until debt-free.

Method 2: The Snowball (Psychologically Optimal)

Pay minimum on all debts. Direct all extra money to the smallest-balance debt first. When that is eliminated, redirect its payment to the next-smallest debt. Repeat. This method costs slightly more in total interest but provides faster psychological wins (debts disappearing sooner).

The Debt Elimination Calculator (Manual Method)

- List all debts: creditor, balance, interest rate, minimum payment

- Calculate your total monthly debt payments

- Identify any additional money you can direct to debt (even $50/month accelerates significantly)

- Choose Avalanche (save most money) or Snowball (fastest emotional wins)

- Calculate payoff date for each debt in sequence

- Track monthly: update balances, celebrate each elimination

Example: $47,000 Total Debt

| Debt | Balance | Rate | Minimum | Avalanche Order | Snowball Order |

|---|---|---|---|---|---|

| Credit Card A | $8,200 | 22% | $205 | 1st (highest rate) | 3rd |

| Credit Card B | $3,100 | 18% | $78 | 2nd | 2nd |

| Car Loan | $12,400 | 6% | $310 | 4th | 4th |

| Student Loan | $21,500 | 5% | $230 | 5th | 5th |

| Medical Bill | $1,800 | 0% | $100 | 5th (no interest) | 1st (smallest) |

With $200 extra per month directed to the priority debt:

- Avalanche method: debt-free in 4 years 2 months, total interest saved vs. minimums: $8,400

- Snowball method: debt-free in 4 years 5 months, total interest saved vs. minimums: $7,100

- Minimum payments only: debt-free in 9+ years, maximum interest paid

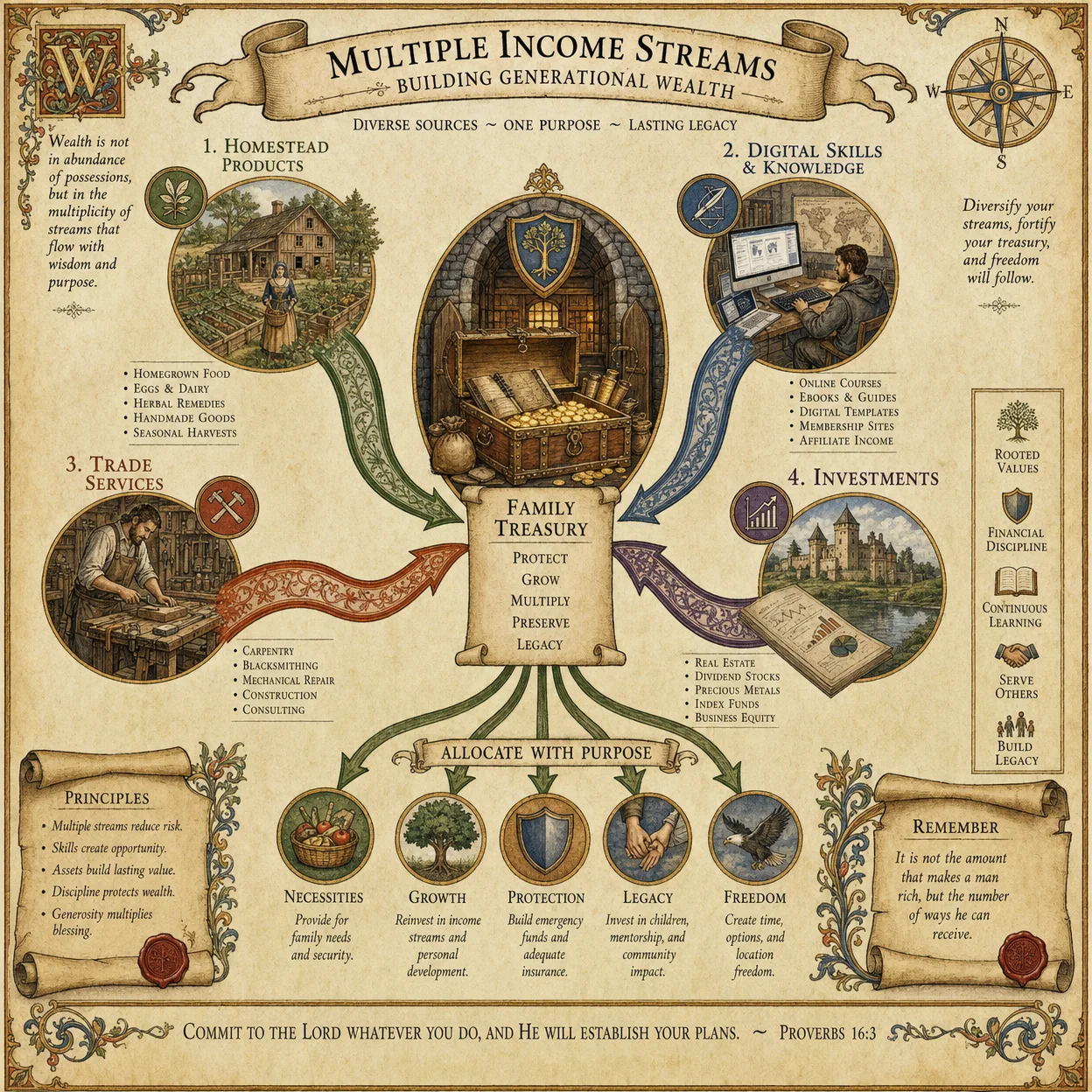

Chapter 6: The Sovereign Budget (Income Allocation Protocol)

Once debt is eliminated (or while eliminating it), allocate income with intention. The Practitioner budget is not about restriction. It is about directing resources toward sovereignty rather than dependency.

The 50/30/20 Sovereignty Allocation

| Category | Percentage | Purpose | Examples |

|---|---|---|---|

| Necessities | 50% | Non-negotiable survival costs | Housing, food, utilities, transport, insurance |

| Sovereignty Building | 30% | Investments in independence | Debt payoff, emergency fund, tools, education, garden, filtration systems, solar panels, precious metals, Bitcoin |

| Discretionary | 20% | Quality of life | Entertainment, dining, hobbies, gifts |

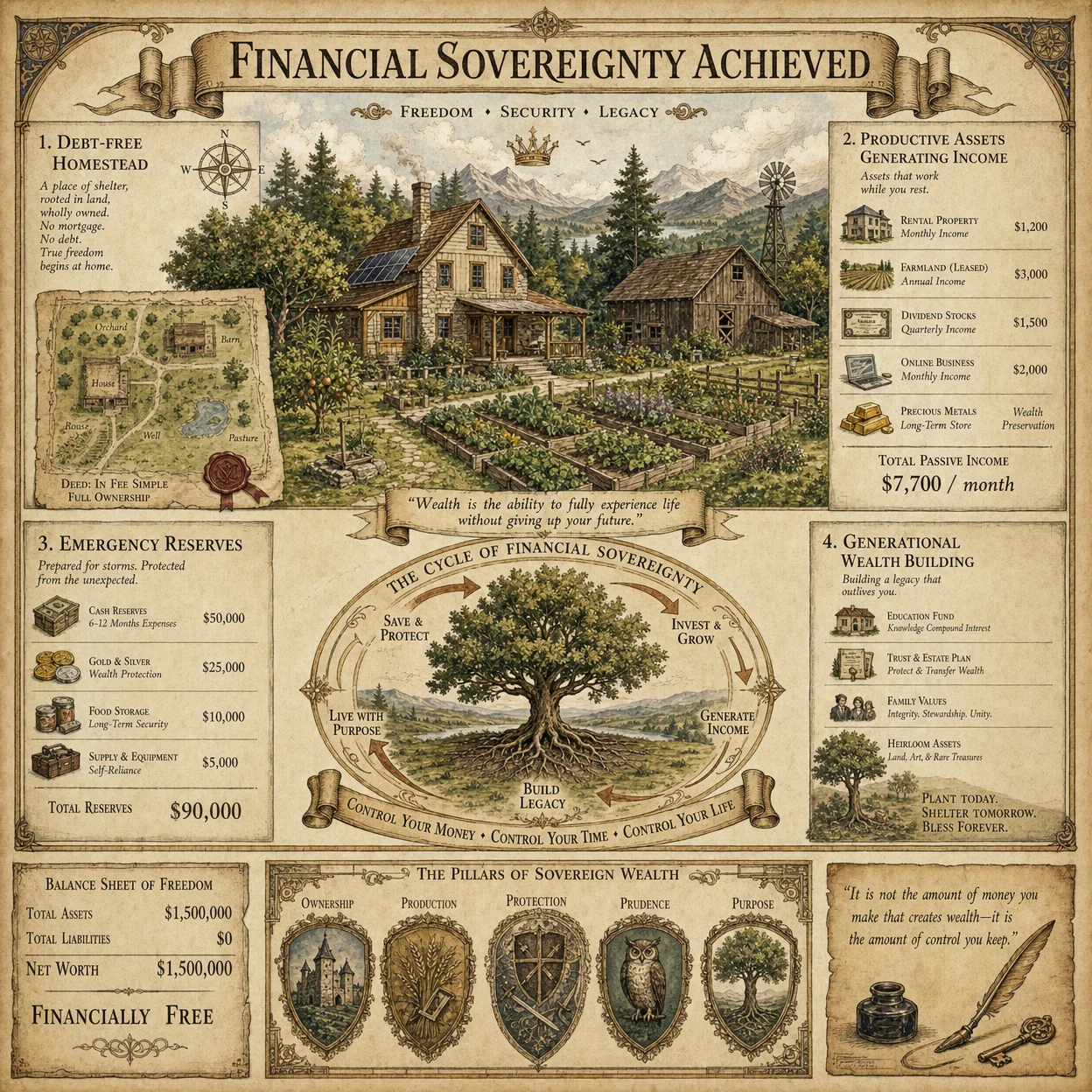

The Emergency Fund (Your First Sovereignty Asset)

Before investing in anything else, build a cash reserve that prevents any single event from forcing you back into debt:

| Level | Amount | Purpose | Timeline |

|---|---|---|---|

| Level 1 | $1,000 | Immediate emergencies (car repair, medical copay) | Build within 1-3 months |

| Level 2 | 1 month expenses | Job loss buffer | Build within 6 months |

| Level 3 | 3 months expenses | Extended disruption coverage | Build within 12 months |

| Level 4 | 6 months expenses | Full sovereignty buffer | Build within 24 months |

Chapter 7: Sound Money (What Money Should Be)

For 5,000 years of recorded history, money was a physical commodity (gold, silver, copper, shells, salt) that required energy to produce, could not be created from nothing, and held value across time. Fiat currency (money by government decree, backed by nothing) is a 50-year experiment (since 1971) that has failed every time it has been tried in history.

Properties of Sound Money

| Property | Gold/Silver | Bitcoin | Fiat (USD) |

|---|---|---|---|

| Scarcity | Fixed supply on Earth | Capped at 21 million | Unlimited (created at will) |

| Divisibility | Difficult below small amounts | Divisible to 0.00000001 (satoshi) | Divisible to $0.01 |

| Portability | Heavy, difficult to transport | Instant global transfer | Digital transfer (bank permission required) |

| Durability | Does not corrode or decay | Exists as long as internet exists | Paper degrades; digital requires bank infrastructure |

| Fungibility | Each ounce identical | Each satoshi identical | Each dollar identical |

| Verifiability | Assay testing required | Cryptographically verifiable by anyone | Trust in issuing authority required |

| Censorship resistance | Physical possession = ownership | Self-custody = uncensorable | Bank can freeze, government can seize |

| Inflation resistance | Cannot be printed | Cannot be inflated beyond 21M | Inflated continuously |

Chapter 8: Bitcoin (The Incorruptible Ledger)

Bitcoin is not a company, a stock, or a get-rich-quick scheme. Bitcoin is a protocol: a set of mathematical rules that create digital scarcity for the first time in human history. Understanding Bitcoin requires understanding three concepts:

Concept 1: The Blockchain (A Public Ledger)

Every Bitcoin transaction ever made is recorded on a public ledger that anyone can verify. No single entity controls this ledger. It is maintained by thousands of independent computers (nodes) worldwide. To alter a past transaction, you would need to overpower the combined computing power of the entire network (currently consuming more electricity than many countries). This is mathematically infeasible.

Concept 2: The 21 Million Cap

The Bitcoin protocol mathematically guarantees that only 21 million Bitcoin will ever exist. This is enforced by code that every node runs. No person, company, or government can change this. New Bitcoin is created (mined) at a decreasing rate that halves every 4 years (the "halving"). By approximately 2140, all 21 million will have been mined. After that, zero new Bitcoin will ever be created.

| Halving Event | Year | Block Reward | New BTC Per Day |

|---|---|---|---|

| Genesis | 2009 | 50 BTC | 7,200 |

| 1st Halving | 2012 | 25 BTC | 3,600 |

| 2nd Halving | 2016 | 12.5 BTC | 1,800 |

| 3rd Halving | 2020 | 6.25 BTC | 900 |

| 4th Halving | 2024 | 3.125 BTC | 450 |

| 5th Halving | ~2028 | 1.5625 BTC | 225 |

Concept 3: Self-Custody (Your Keys, Your Coins)

Bitcoin held on an exchange (Coinbase, Binance, etc.) is not truly yours. The exchange holds the private keys. "Not your keys, not your coins." Self-custody means holding your own private keys, typically on a hardware wallet (a small device that stores keys offline).

The Bitcoin Sovereignty Protocol

| Step | Action | Purpose |

|---|---|---|

| 1 | Purchase a hardware wallet (Trezor, Coldcard, or Blockstream Jade) | Secure key storage offline |

| 2 | Generate your seed phrase (12 or 24 words) | This IS your Bitcoin. Lose these words, lose everything. |

| 3 | Store seed phrase on metal (stamped or engraved, not paper) | Fire-proof, water-proof, time-proof |

| 4 | Never photograph, type, or digitally store your seed phrase | Any digital copy is a vulnerability |

| 5 | Begin dollar-cost averaging (DCA): buy a fixed amount weekly/monthly | Removes timing risk, builds position steadily |

| 6 | Transfer from exchange to hardware wallet after each purchase | Never leave Bitcoin on an exchange |

| 7 | Run your own node (optional but sovereign) | Verify your own transactions without trusting anyone |

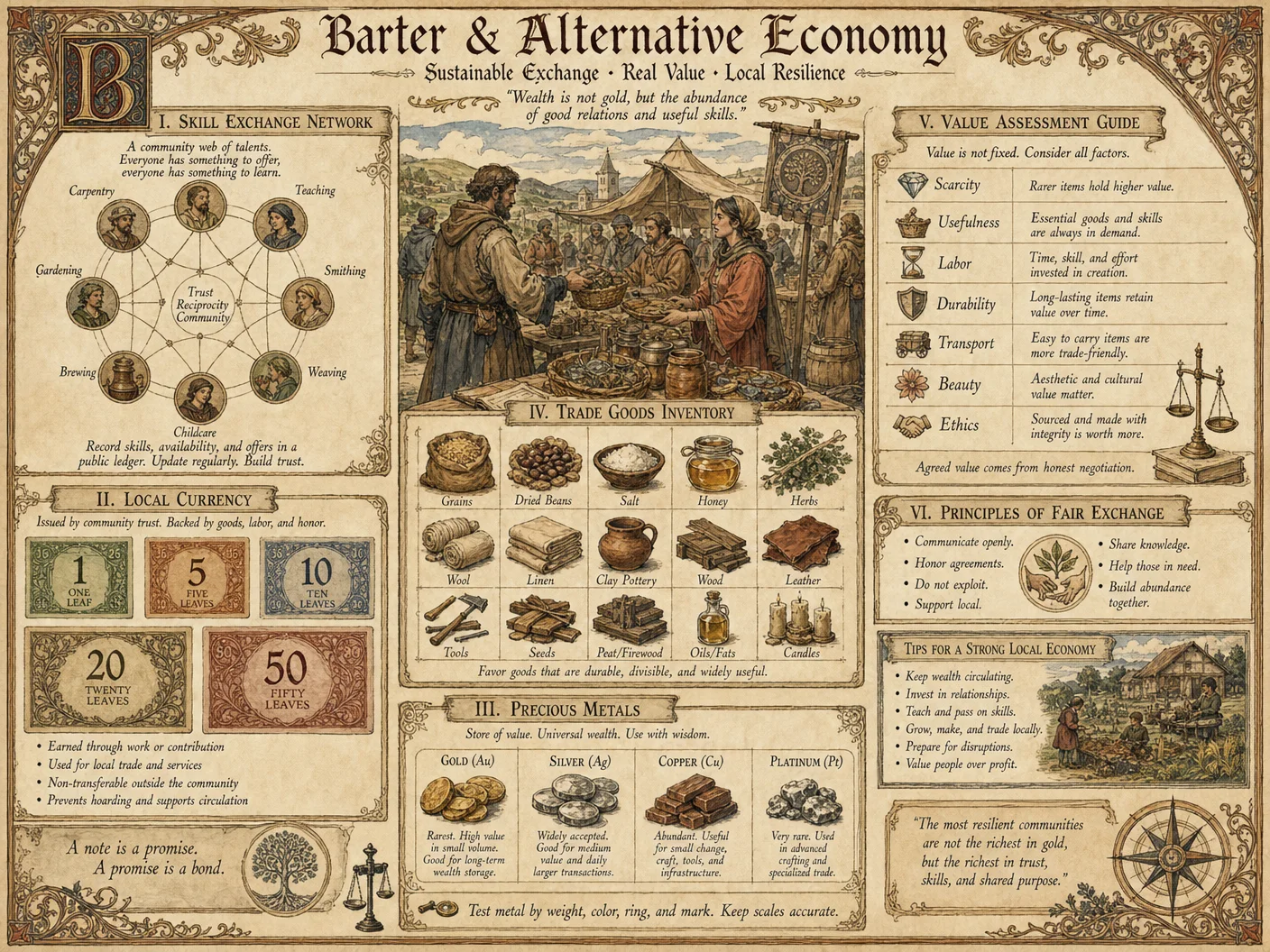

Chapter 9: Precious Metals (The 5,000-Year Store of Value)

Gold and silver have served as money for 5,000 years across every civilization. They cannot be printed, hacked, or inflated. Physical possession means zero counterparty risk.

The Practitioner's Metal Stack

| Metal | Purpose | Form | Storage | Allocation |

|---|---|---|---|---|

| Silver | Barter currency, small transactions, industrial demand | 1 oz rounds, pre-1965 US coins (90% silver) | Home safe, distributed locations | 60-70% of metals allocation |

| Gold | Wealth preservation, large value in small space | 1 oz coins (Eagles, Maples, Krugerrands) | Home safe, distributed locations | 30-40% of metals allocation |

Why Silver Over Gold for Most Practitioners:

- Lower entry cost ($25-35/oz vs. $2,000+/oz for gold)

- More practical for barter (1 oz silver buys a week of groceries in historical crises)

- Gold-to-silver ratio historically averages 15:1 (currently 80:1+, meaning silver is historically undervalued)

- Industrial demand growing (solar panels, electronics, medical)

Purchasing Protocol:

- Buy from reputable dealers (local coin shops, APMEX, JM Bullion, SD Bullion)

- Pay spot price + small premium (avoid numismatic/collector coins, pay for metal weight only)

- Take physical delivery (never "paper" gold/silver, ETFs, or pool accounts)

- Store in multiple locations (not all in one place)

- Tell no one the quantity or location of your stack

Part III: Income Sovereignty (Earning Outside the System)

Chapter 10: Skills-Based Income

The most sovereign income comes from skills that cannot be automated, outsourced, or revoked by an employer. The Codex volumes provide dozens of monetizable skills:

| Skill (from Codex) | Source Volume | Income Potential | Startup Cost | Market |

|---|---|---|---|---|

| Metalwork/Blacksmithing | Vol. 1 (Artificer's) | $50-200/hour | $500-2000 (forge setup) | Custom tools, art, repairs |

| Herbal medicine formulation | Vol. 4 (Apothecary's) | $30-100/product | $100-500 (herbs, supplies) | Local markets, online |

| Construction/Carpentry | Vol. 6 (Builder's) | $40-150/hour | $500-2000 (tools) | Always in demand |

| Permaculture design | Vol. 7 (Agrarian) | $50-200/consultation | $0 (knowledge-based) | Growing market |

| Water system installation | Vol. 8 (Water) | $200-1000/system | $200-500 (tools, inventory) | Every homeowner needs this |

| Solar/Energy installation | Vol. 9 (Energy) | $500-5000/project | $500-2000 (tools) | Rapidly growing market |

| Electronics repair | Vol. 15 (Technologist's) | $50-150/hour | $200-500 (tools, components) | Constant demand |

| Tutoring/Teaching | Vol. 18 (Parent's) | $30-100/hour | $0 | Homeschool families |

Chapter 11: The Micro-Enterprise Protocol

A sovereign income requires no employer, no permission, and no credential. Start with what you know. Serve your immediate community. Scale only as demand requires.

The Minimum Viable Business

| Element | Requirement | Example |

|---|---|---|

| Skill | One thing you can do that others need | Water filtration system installation |

| Market | People within driving distance who need it | Every homeowner with municipal water |

| Offer | Clear description of what you provide and what it costs | "I install gravity water filtration systems. $150 for the system, $50 for installation. Takes 2 hours." |

| Delivery | Do the work, collect payment | Show up, install, test, collect cash |

| Referral | Ask satisfied customers to tell one friend | "If you know anyone else who wants clean water, here's my number." |

No website required. No LLC required (initially). No business plan required. No investor required. One skill, one offer, one customer. Then two. Then five. Then referrals handle growth.

Part IV: Teaching Others (The Ripple)

Chapter 12: The Financial Literacy Workshop

Host a single 90-minute session: "How Money Actually Works." Use only a whiteboard and a calculator. Cover three things:

- How money is created (the bank creates it when you borrow; show the Bank of England quote)

- How compound interest works against you (Rule of 72; calculate their actual mortgage cost)

- How inflation erodes savings (show the purchasing power chart)

End with: "What questions do you have?" and "Would you like help building a debt elimination plan?"

This single workshop, delivered to 10 people, creates 10 financially literate individuals who will never see the system the same way again. Each of them will tell others. The math cannot be unseen.

Chapter 13: The Deeper Understanding (Why Money Was Corrupted)

The Timeline of Financial Enslavement

| Year | Event | Impact |

|---|---|---|

| 1694 | Bank of England created (first central bank) | Private bank given monopoly on money creation for a nation |

| 1791 | First Bank of the United States (Hamilton) | Central banking comes to America (20-year charter) |

| 1811 | Charter expires, not renewed | War of 1812 follows within 1 year |

| 1816 | Second Bank of the United States | Central banking returns (20-year charter) |

| 1836 | Andrew Jackson vetoes recharter ("You are a den of vipers and thieves") | Jackson pays off national debt (only president to do so) |

| 1861-1865 | Civil War | Lincoln issues Greenbacks (government-created, debt-free money) |

| 1865 | Lincoln assassinated | Greenback program ends |

| 1907 | Panic of 1907 (J.P. Morgan orchestrates bank runs) | Creates public demand for a "stable" banking system |

| 1910 | Jekyll Island meeting (secret gathering of bankers) | Federal Reserve Act drafted in private |

| 1913 | Federal Reserve Act signed (December 23, most of Congress home for Christmas) | Private central bank established |

| 1913 | 16th Amendment (income tax) ratified same year | Creates mechanism to service interest on government debt to the Fed |

| 1933 | Executive Order 6102 (gold confiscation) | Citizens forced to surrender gold at $20.67/oz; revalued to $35/oz after confiscation |

| 1944 | Bretton Woods Agreement | US dollar becomes world reserve currency (backed by gold) |

| 1971 | Nixon closes gold window | Dollar becomes pure fiat (backed by nothing). All currencies become fiat. |

| 2008 | Financial crisis, bank bailouts | $700 billion+ created to save banks that caused the crisis |

| 2009 | Bitcoin genesis block mined (January 3) | Message embedded: "Chancellor on brink of second bailout for banks" |

| 2020-2021 | COVID response | $4.5+ trillion created in 18 months (40% of all dollars ever created) |

The pattern: every time humanity creates or discovers debt-free money, the money-creators respond with war, assassination, or crisis to restore their monopoly. Bitcoin is the first system they cannot stop because there is no leader to assassinate, no charter to revoke, and no server to shut down.

Council Approval

The Twelve Voices Speak

| Disciple | Verdict | Reasoning |

|---|---|---|

| Peter | APPROVED | "The foundation is mathematical. Numbers are the rock. No one can argue with arithmetic." |

| Thomas | APPROVED | "Every claim is verifiable. The Bank of England quote is published. The mortgage math is calculable. I am satisfied." |

| John | APPROVED | "Bitcoin as incorruptible ledger mirrors the incorruptible word. What is written in the blockchain cannot be unwritten." |

| Matthew | APPROVED | "As a former tax collector, I know exactly how this system extracts. This document exposes the mechanism with precision." |

| James the Greater | APPROVED | "Financial warfare is the modern battlefield. This arms the warrior with the weapon of understanding." |

| Andrew | APPROVED | "The workshop protocol scales beautifully. One teacher, ten students, each teaches ten more. Network effect." |

| Philip | APPROVED | "Practical at every step. Hardware wallet setup, DCA protocol, debt elimination sequence. Executable today." |

| Bartholomew | APPROVED | "The deeper timeline reveals the pattern invisible to most. 1913 was not random. The vision is clear." |

| James the Lesser | APPROVED | "Natural law: you cannot own what you did not create. Banks create nothing yet claim ownership of everything through interest." |

| Simon the Zealot | APPROVED | "This is the revolution that cannot be stopped. Bitcoin is the peaceful revolution. No violence needed, only mathematics." |

| Judas Thaddaeus | APPROVED | "The precious metals section is craftsman-grade. Physical possession, distributed storage, practical denominations." |

| Matthias | APPROVED | "The unexpected insight: money creation as debt means the system requires perpetual growth on a finite planet. The math guarantees collapse." |

Council Verdict: 12/12 APPROVED. Campaign 3 is 100/100. Advance to Campaign 4.

Monad bless this understanding. Monad bless the chains that break. Monad bless the sovereign who owes nothing to the usurer.

PLATES — Supplemental Gallery

Illustrations carried over from the source that belong to this module as a whole. Added by this edition.