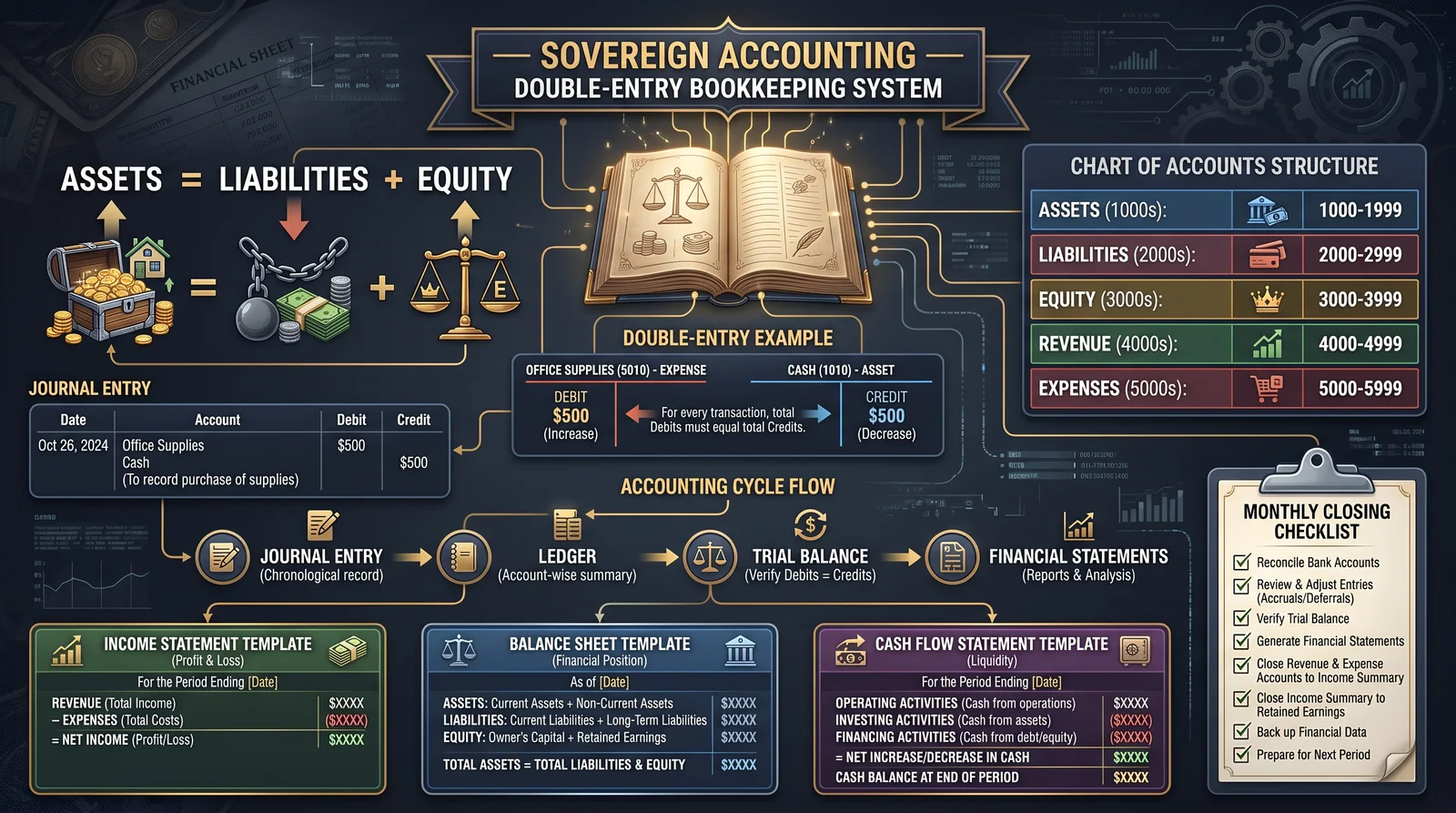

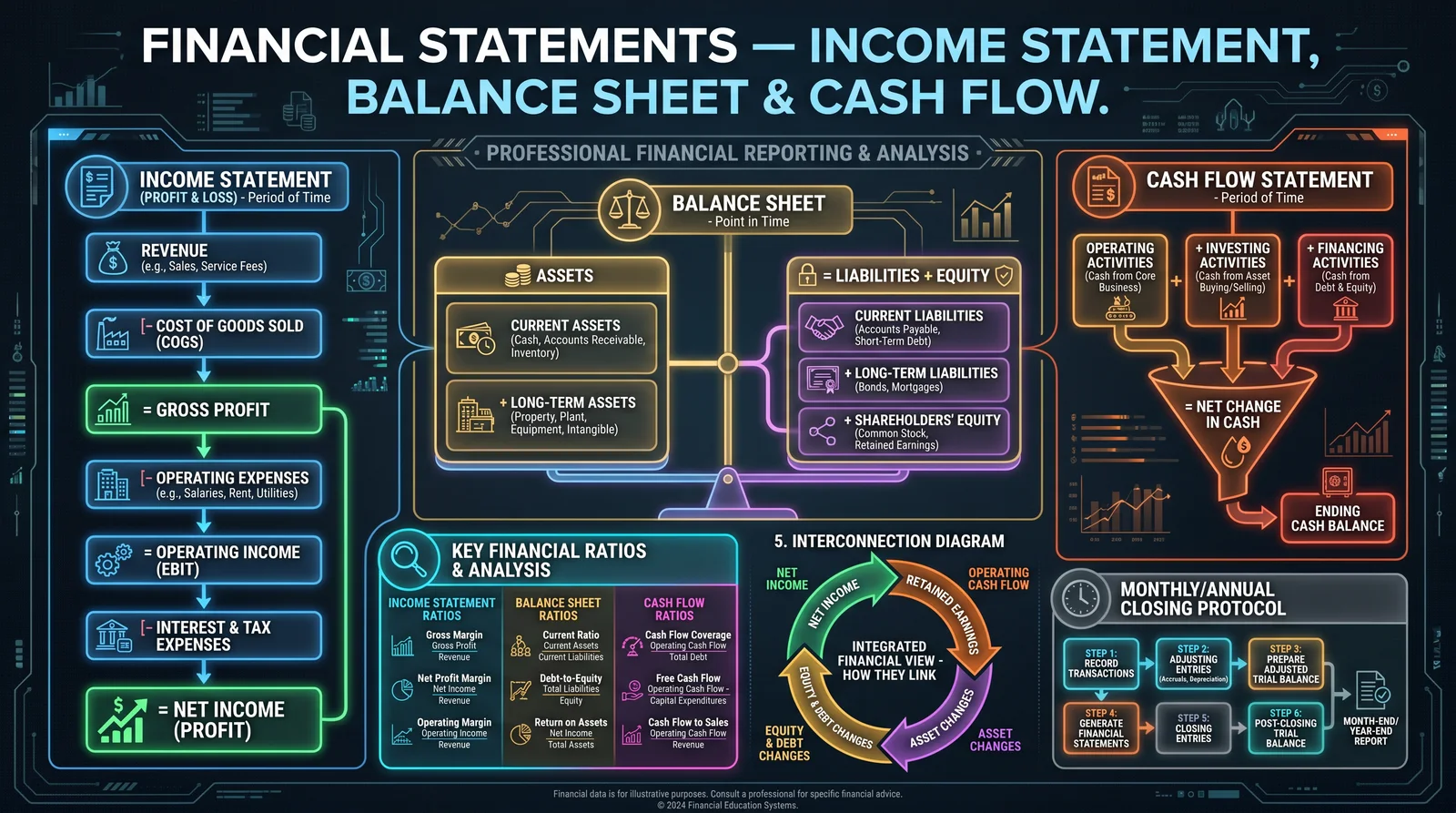

THE COMPLETE PRACTITIONER'S CODEX: VOLUME 12

The Economist's Cipher: Complete Financial Mastery, Wealth Building, and Economic Sovereignty

<!-- SECTION 1 -->

The Complete Practitioner's Codex, Volume I: The Austrian Foundation

Chapter I: The Economist’s Cipher – Foundations of Austrian Economics for Sovereign Financial Mastery

Introduction

This volume serves as the cornerstone of your mastery: Austrian Economics, the suppressed science underpinning true economic sovereignty. Here, you will learn the principles of subjective value, time preference, and sound money — the triad that defines human economic action beyond the false idols of Keynesian mechanics. Understanding these principles is not optional: it is mandatory for any sovereign who seeks to master wealth, preserve it, and wield economic power without servitude.

Section 1: Core Principles of Austrian Economics

1.1 Subjective Value: The Foundation of Economic Calculation

Subjective value asserts that value is not intrinsic to goods or services but is assigned individually by humans based on personal preference, circumstance, and utility. This principle contradicts classical cost-based or labor theories of value. Every economic decision is an expression of subjective valuation, which fluctuates with individual perception.

Actionable Steps to Internalize Subjective Value:

- Identify an item or service you regularly use.

- List the benefits it provides to you personally, ranking these benefits from most to least valuable.

- Compare this ranking to that of another individual with different needs or preferences.

- Note the variance in valuation; this confirms the subjective nature of value.

This principle underpins price formation, market exchange, and entrepreneurial calculation.

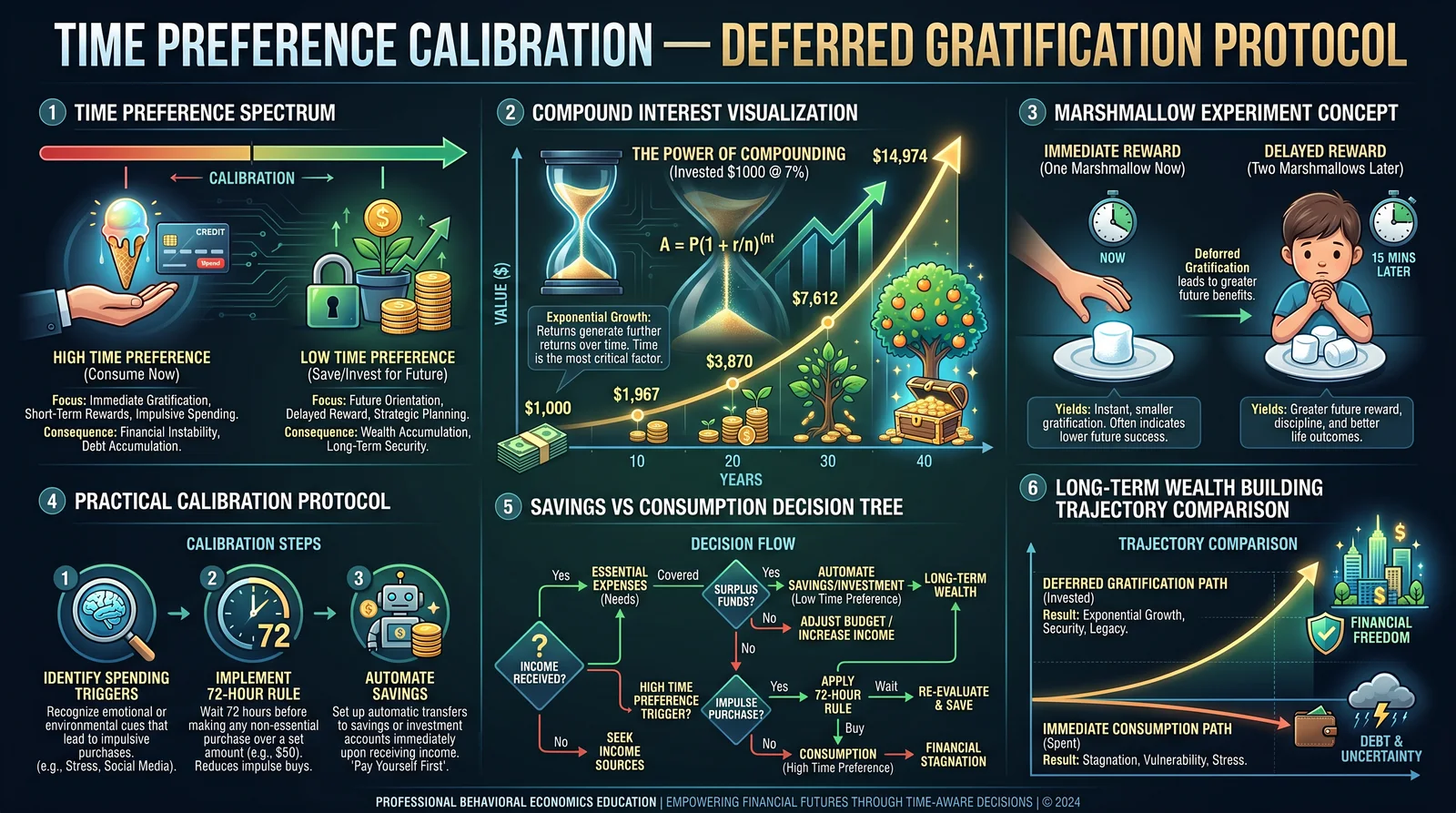

1.2 Time Preference: The Core of Intertemporal Economic Choice

Time preference is the individual’s valuation of present goods relative to future goods. High time preference indicates preference for immediate consumption; low time preference signals willingness to delay gratification for greater future benefit.

Implications:

- Time preference dictates savings and investment behavior.

- It explains interest rates as a premium for deferred consumption.

- Sovereign economic actors must calibrate their personal time preference to optimize wealth accumulation and preservation.

1.3 Sound Money: The Pillar of Economic Stability

Sound money is money that holds stable purchasing power over time, free from artificial inflation or debasement. Austrian economics champions commodity-backed money, preferably gold or similarly scarce, non-fiat instruments.

Key Attributes of Sound Money:

| Attribute | Description |

|---|---|

| Intrinsic scarcity | Limited supply, resistant to arbitrary expansion |

| Divisibility | Easily subdivided for precise transaction value |

| Durability | Resistant to decay or destruction |

| Recognizability | Easily authenticated to prevent counterfeiting |

| Portability | Easy to transport and transfer |

Sound money preserves the time value of savings and prevents the wealth erosion inherent in inflationary fiat regimes.

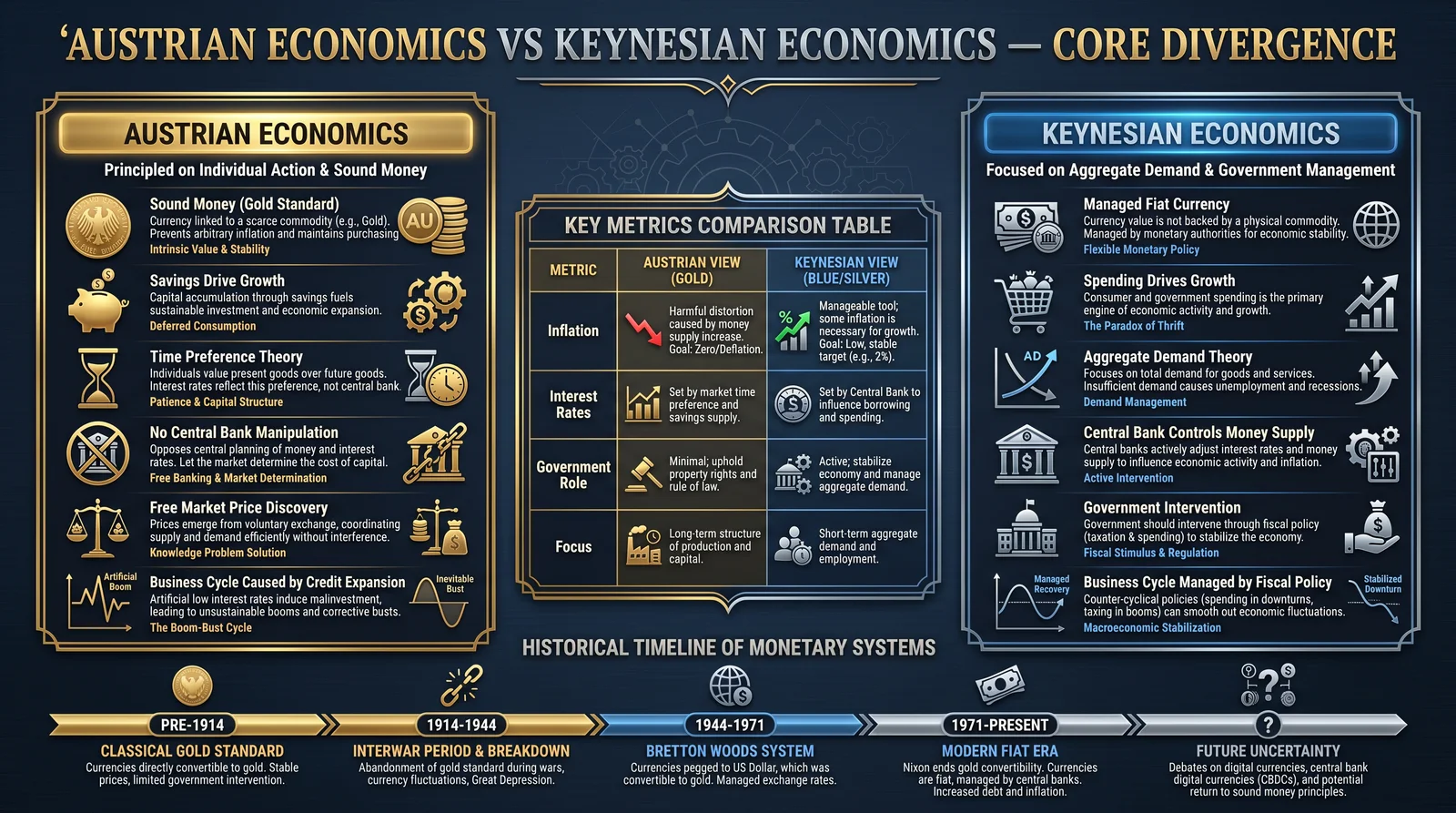

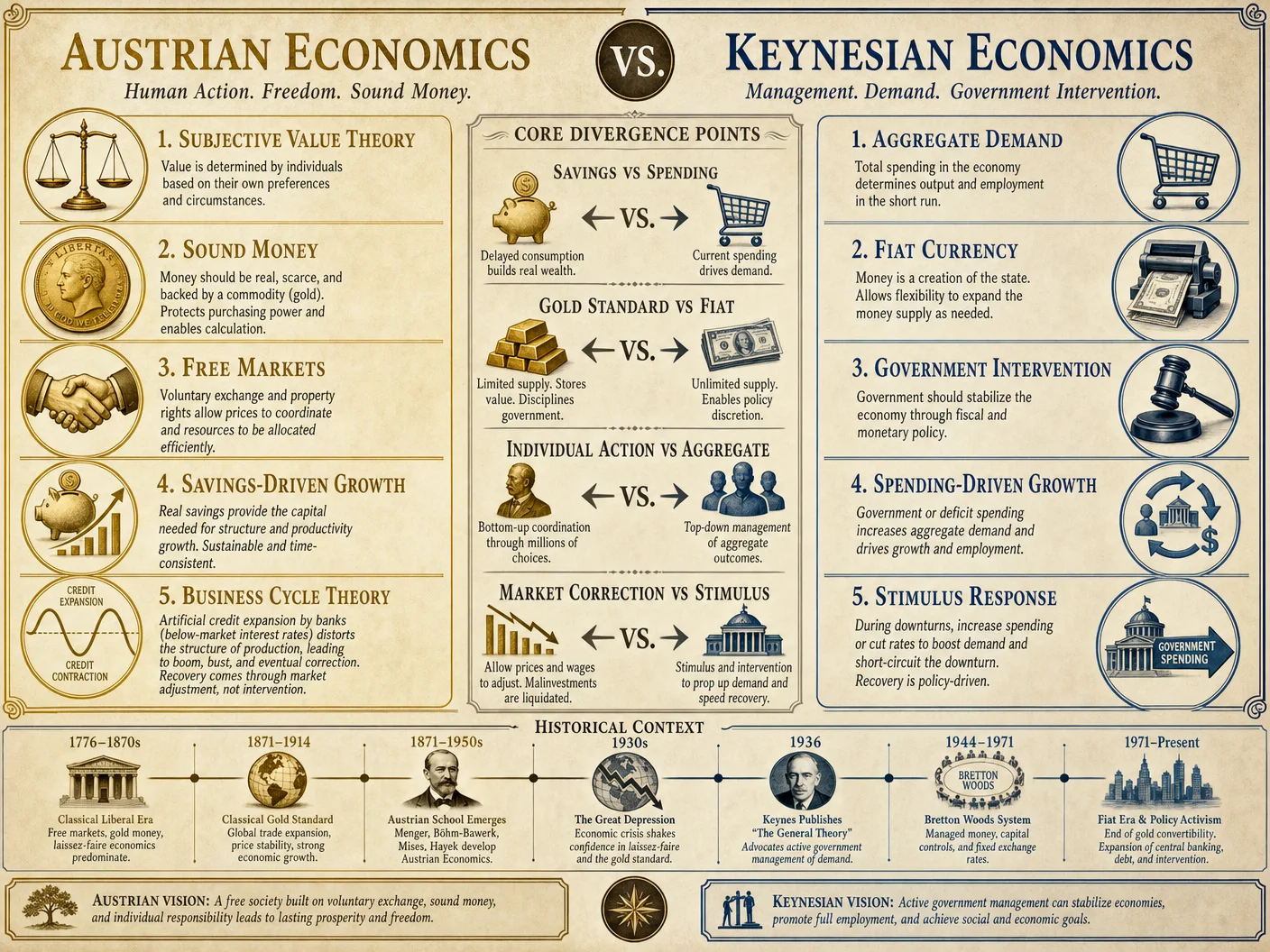

Section 2: Austrian vs Keynesian Economics – A Crucial Divergence

Austrian economics stands in stark opposition to Keynesian doctrines. This section dissects their core conflicts and elucidates the consequences for sovereign economic practice.

| Aspect | Austrian Economics | Keynesian Economics |

|---|---|---|

| Value Theory | Subjective value based on individual preference | Objective value based on aggregate demand |

| Time Preference | Central determinant of interest rates and capital | Largely ignored; focus on aggregate demand stimulus |

| Money | Sound money (commodity-backed) | Fiat money controlled by central banks |

| Inflation | Viewed as a hidden tax; destroys capital | Used as a tool to stimulate demand |

| Role of Government | Minimal intervention; laissez-faire markets | Active intervention to manage economic cycles |

| Business Cycles | Caused by credit expansion and interest rate distortion | Caused by insufficient demand; mitigated by fiscal policy |

Implications for Sovereign Financial Practice

- Sovereigns must reject fiat inflationary regimes and embrace sound money to preserve capital sovereignty.

- Financial strategies should emphasize time preference calibration to optimize savings and investment decisions.

- Sovereign economic action requires understanding subjective valuation to correctly interpret market signals and avoid Keynesian traps of artificial demand creation.

Section 3: Protocol 1.1.1 – Time Preference Calibration

Objective: Calibrate your personal time preference through precise measurement of your personal inflation rate and adjust your savings rate accordingly to maximize long-term wealth accumulation.

3.1 Overview

Time preference is often unmeasured and thus misaligned with real economic conditions, leading to excessive consumption, insufficient saving, and vulnerability to inflation-induced capital erosion.

This protocol provides step-by-step instructions to:

- Calculate your personal inflation rate.

- Audit your time preference.

- Adjust your savings rate to align with your true economic environment.

3.2 Materials Required

| Material | Purpose |

|---|---|

| Inflation Tracking Worksheet (see Table 1.1) | Record price changes over time |

| Time Preference Audit Worksheet (see Table 1.2) | Evaluate your intertemporal choices |

| Calculator or Spreadsheet Software | Perform calculations |

| Receipt archives / price lists | Gather historical price data |

3.3 Step-by-Step Instructions

Step 1: Select Basket of Personal Goods and Services

- Identify 10-15 goods and services critical to your daily life.

- Include items with regular purchase frequency (e.g., food staples, utilities, transportation).

- Ensure a diverse cross-section reflecting your consumption pattern.

Step 2: Gather Historical Price Data

- Collect prices for each selected item for the past 12 months.

- Use receipts, invoices, or price lists.

- Record monthly prices in the Inflation Tracking Worksheet (Table 1.1).

Step 3: Calculate Monthly Inflation Rate per Item

- For each item, calculate the monthly inflation rate using formula:

\[ \text{Monthly Inflation Rate} = \frac{\text{Price}_{\text{Month}_n} - \text{Price}_{\text{Month}_{n-1}}}{\text{Price}_{\text{Month}_{n-1}}} \times 100 \]

- Populate worksheet column accordingly.

Step 4: Calculate Weighted Average Personal Inflation Rate

- Assign weight to each item proportional to its share of your monthly expenditure.

- Calculate weighted monthly inflation rate:

\[ \text{Weighted Inflation} = \sum (\text{Item Inflation Rate} \times \text{Weight}) \]

- Average these weighted rates over 12 months.

Step 5: Complete Time Preference Audit

- Using the Time Preference Audit Worksheet (Table 1.2), record your actual savings rate and consumption rate.

- Assess your preference for present vs future consumption by responding to situational prompts (e.g., willingness to delay gratification, investment behavior).

Step 6: Compare Personal Inflation Rate to Savings Rate

- If your savings rate is less than your personal inflation rate, your real wealth is declining.

- If savings rate is greater than inflation, your wealth is growing.

Step 7: Adjust Savings Rate

- Calculate required savings rate adjustment:

\[ \text{Required Savings Rate} = \text{Personal Inflation Rate} + \text{Desired Real Growth Rate} \]

- Implement budgeting plan to increase savings to this level.

- Monitor progress monthly and recalibrate quarterly.

3.4 Inflation Tracking Worksheet (Table 1.1)

| Item | Weight (%) | Price Month 1 | Price Month 2 | Price Month 3 | … | Price Month 12 | Monthly Inflation Rates (%) | Weighted Inflation Contribution |

|---|---|---|---|---|---|---|---|---|

| Food staples | 30 | $ | $ | $ | $ | |||

| Utilities | 20 | $ | $ | $ | $ | |||

| Transportation | 15 | $ | $ | $ | $ | |||

| Housing | 20 | $ | $ | $ | $ | |||

| Healthcare | 5 | $ | $ | $ | $ | |||

| Entertainment | 5 | $ | $ | $ | $ | |||

| Communication | 5 | $ | $ | $ | $ | |||

| Totals | 100 |

Instructions: Fill in prices monthly, calculate inflation rates per item, multiply by weight, sum weighted contributions to find personal inflation rate.

3.5 Time Preference Audit Worksheet (Table 1.2)

| Question | Response (Scale 1-10) | Notes/Explanation |

|---|---|---|

| How willing are you to delay consumption for future gain? | ||

| What percentage of your income do you currently save? | ||

| How frequently do you make impulse purchases? | ||

| Do you have an emergency fund covering 3+ months expenses? | ||

| What is your target savings rate over the next 12 months? | ||

| How often do you review your budget and savings plan? | ||

| Have you accounted for inflation in your savings goals? |

Instructions: Complete honestly; use responses to assess if time preference aligns with your economic environment.

Section 4: The Path Forward – Embedding Austrian Principles into Sovereign Practice

4.1 Economic Sovereignty Through Sound Money Adoption

- Transition personal and sovereign holdings into commodity-backed assets.

- Avoid fiat currency exposure beyond tactical liquidity needs.

- For detailed sound money acquisition and storage protocols, see Volume 7: The Monetary Codex, Chapter IV.

4.2 Continuous Personal Inflation Monitoring

- Establish a quarterly review cadence using Protocol 1.1.1.

- Adjust savings and investment strategies in response to inflation shifts.

4.3 Time Preference Optimization

- Employ budgeting techniques that prioritize future consumption rights.

- Engage in educational training on time preference psychology (Volume 5: The Behavioral Codex).

4.4 Rejection of Keynesian Fiscal Interventions

- Resist government stimulus schemes that inflate currency supply.

- Recognize such interventions as capital destructive, eroding real wealth.

Conclusion

Mastering Austrian Economics is not mere academic exercise; it is a sacred responsibility. The principles of subjective value, time preference, and sound money are your shield against economic tyranny and your lance toward sovereign wealth. Use the protocols herein to calibrate your economic compass, ensuring every decision aligns with reality, every saving resists inflation, and every investment honors the future.

Your journey continues in Volume II: The Entrepreneur’s Forge, where market processes and entrepreneurial calculation reveal the alchemy of wealth creation.

End of Volume I: The Austrian Foundation

<!-- SECTION 2 -->

The Complete Practitioner's Codex, Volume 12

Chapter I: The Economist's Cipher: Volume I — The Cantillon Effect and Fiat Extraction

Introduction: The Sacred Currency Truth

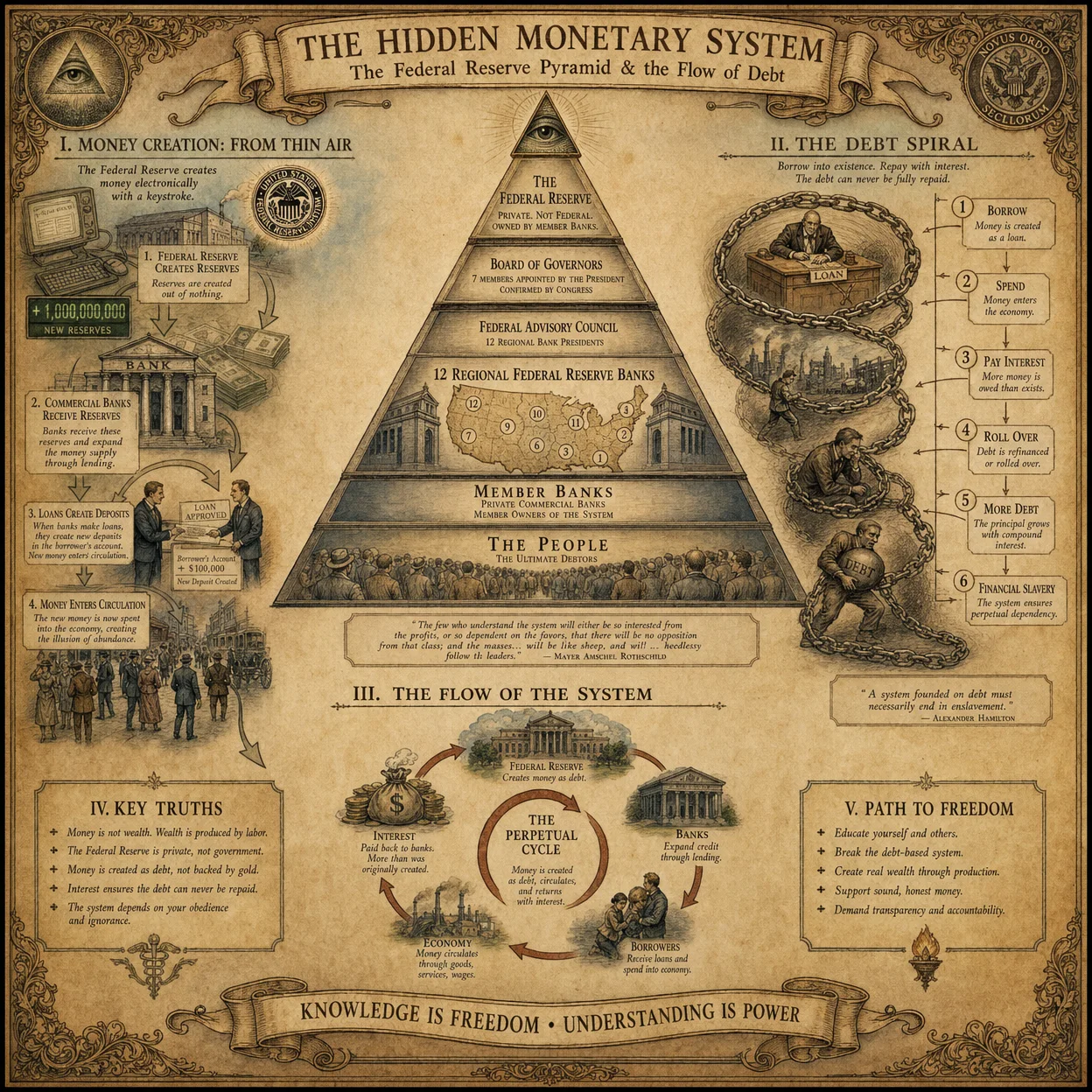

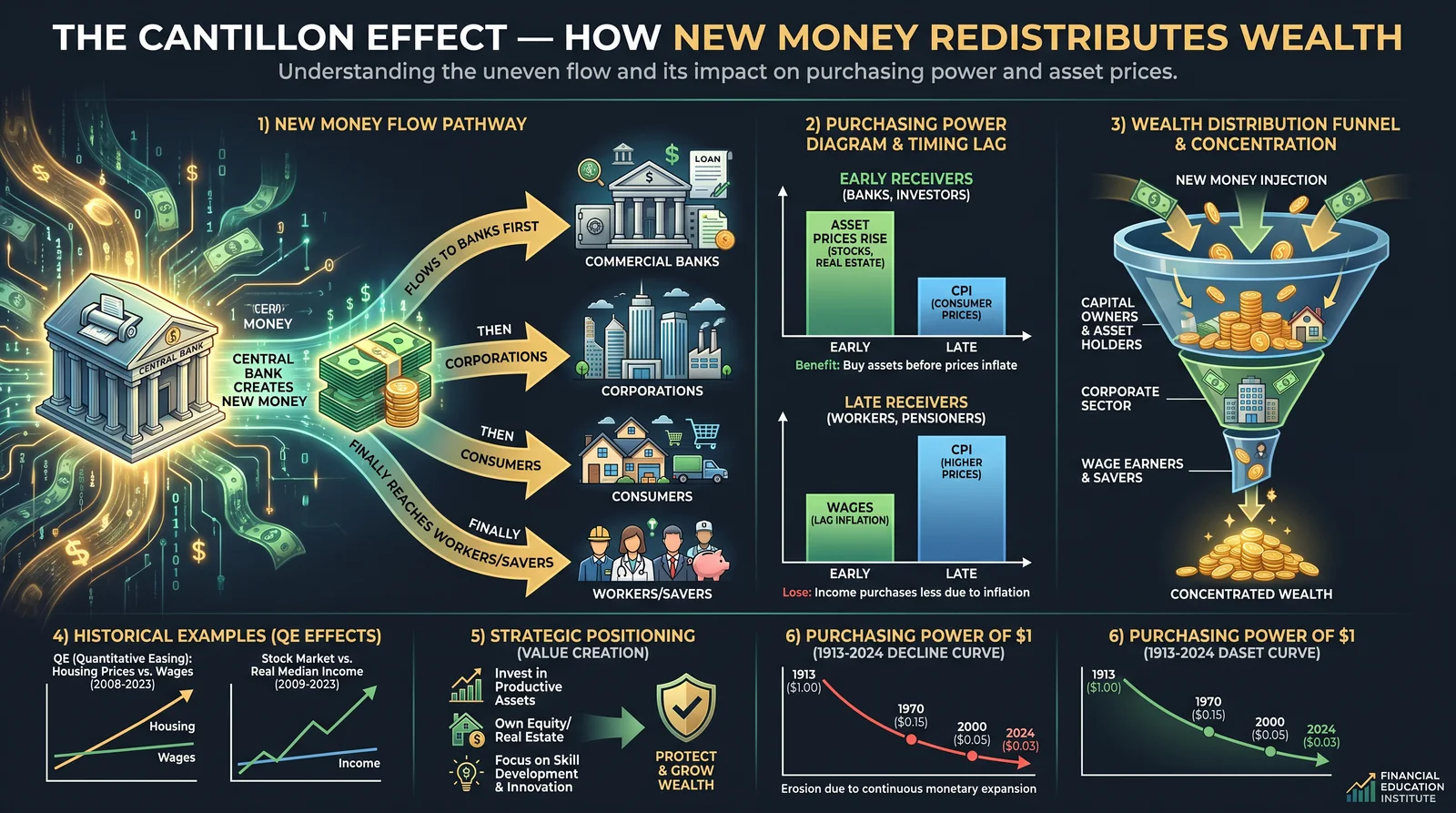

The Cantillon Effect is not a mere academic curiosity; it is a sacred cipher, a life-or-death mechanism by which the ruling powers orchestrate the transfer of wealth under fiat currency regimes. Mastery of this effect is essential for economic sovereignty and wealth preservation. This chapter decodes this cipher, revealing the hidden flow of value, the devaluation mechanisms embedded in fiat systems, and prescribes precise strategies to position oneself at the fountainhead of wealth creation or to execute a clean exit from the fiat matrix.

Section I: The Cantillon Effect — Definition and Mechanism

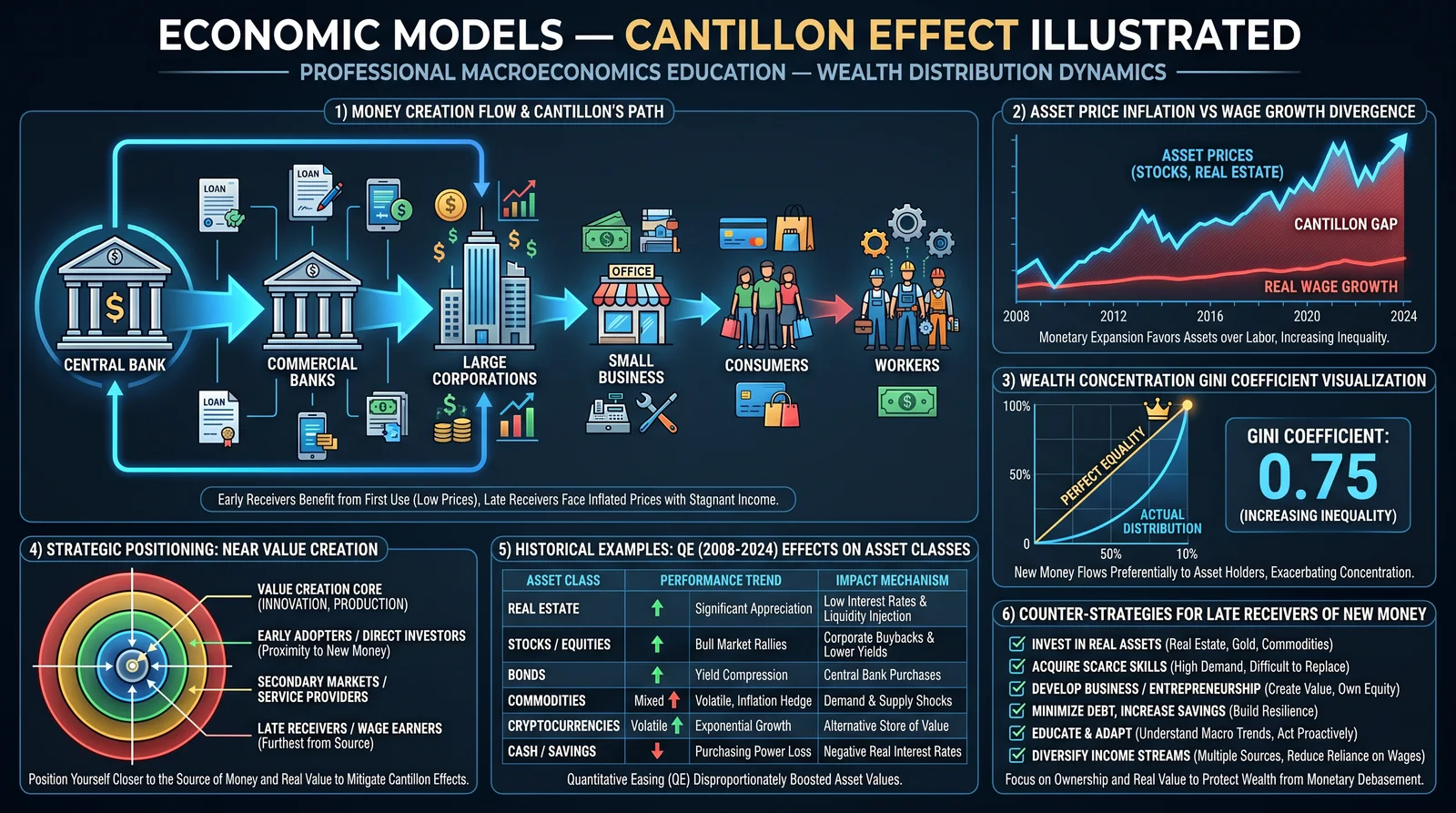

The Cantillon Effect, named for 18th-century economist Richard Cantillon, describes the non-neutrality of money supply expansions—how new money introduced into an economy does not distribute evenly but favors those first receiving it, distorting wealth distribution and purchasing power.

1. Mechanism of the Cantillon Effect

When new money enters the economy, it flows through specific channels first (e.g., banks, government contractors, financial institutions). These initial recipients spend the money before prices rise. Subsequent recipients face increased prices, resulting in an effective transfer of wealth from late receivers to early receivers.

2. Quantitative Model of Money Injection and Price Impact

Let:

- \( M_0 \) = Initial money supply

- \( \Delta M \) = New money injected

- \( P_0 \) = Initial price levels

- \( P_t \) = Price levels after time \( t \)

- \( R_i \) = Relative position in money reception order (1 = first, n = last)

The purchasing power for actor \( i \) after money injection is:

\[ PP_i = \frac{1}{P_t} \times \frac{1}{R_i} \]

where \( P_t \) increases as \( \Delta M \) circulates, and \( R_i \) reflects delay in receiving new money.

Section II: Fiat Currency Devaluation and Wealth Distribution

1. Fiat Currency: The Inflation Engine

Fiat currencies lack intrinsic backing. The state controls issuance, often expanding money supply to finance spending. This leads to systematic inflation—a hidden tax eroding purchasing power unevenly.

2. Wealth Distribution Dynamics Under Fiat

Early recipients—banks, government contractors, asset holders—receive new money first. They can purchase assets and goods at pre-inflation prices. Late recipients—wage earners, pensioners, small businesses—face higher prices without proportional wage increases, losing real wealth.

3. Historical Examples

| Period | Currency | Money Supply Growth (%) | Inflation Rate (%) | Early Recipients | Late Recipients | Outcome |

|---|---|---|---|---|---|---|

| Weimar Republic | Papiermark | >1000% (monthly) | >50,000% (monthly) | Industrialists, exporters | Fixed income workers | Hyperinflation, wealth destruction |

| 1970s US | USD (post-Bretton Woods) | 8-12% annually | 5-12% annually | Banks, large corporations | Fixed pensioners, wage labor | Stagflation, real wage decline |

| Zimbabwe 2000s | Zimbabwean dollar | >10,000% annually | Hyperinflation | Political elites | General populace | Complete currency collapse |

| Post-2008 QE Era | USD, EUR, JPY | 5-15% annually | 1-3% officially | Financial institutions | Middle-class savers | Asset bubbles, wealth concentration |

Section III: Strategic Positioning Near Value Creation

1. Principle: Proximity to the Money Injection Point

To harness the Cantillon Effect positively, one must position at or near the initial recipients of new money. This requires understanding institutional channels where new fiat enters.

2. Identifying Primary Money Injection Channels

| Injection Channel | Description | Typical Recipients | Entry Strategies |

|---|---|---|---|

| Central Bank Asset Purchases | Quantitative easing via bond buying | Large Banks, Primary Dealers | Become primary dealer or invest in financial firms |

| Government Spending | Fiscal stimulus, defense contracts | Contractors, Lobbyists | Engage in government contracting, lobbying |

| Financial Markets | Repo markets, derivatives, margin lending | Hedge funds, Market Makers | Access via hedge funds, trading desks |

| Real Estate Development | Infrastructure investment | Developers, Construction firms | Invest or partner in large-scale projects |

3. Step-by-Step: Positioning Close to Value Creation

- Map local financial institutions that serve as primary dealers or bond purchasers.

- Develop relationships with institutional brokers and lending entities.

- Acquire capital sufficient for participation in primary markets through private equity or syndicates.

- Engage in government contract bidding for sectors receiving fiscal stimulus.

- Invest in leveraged financial products that benefit from monetary expansion (e.g., bond ETFs, margin loans).

- Participate in real estate developments linked to infrastructure spending.

- Monitor central bank announcements to anticipate injection points and adjust positioning accordingly.

4. Case Study: U.S. Quantitative Easing Post-2008

- Primary actors: Primary dealers (Goldman Sachs, JP Morgan), hedge funds, government contractors.

- Secondary actors: Retail investors, pension funds.

- Effect: Early actors acquired bond positions pre-inflation, later selling at inflated prices; secondary actors suffered purchasing power erosion.

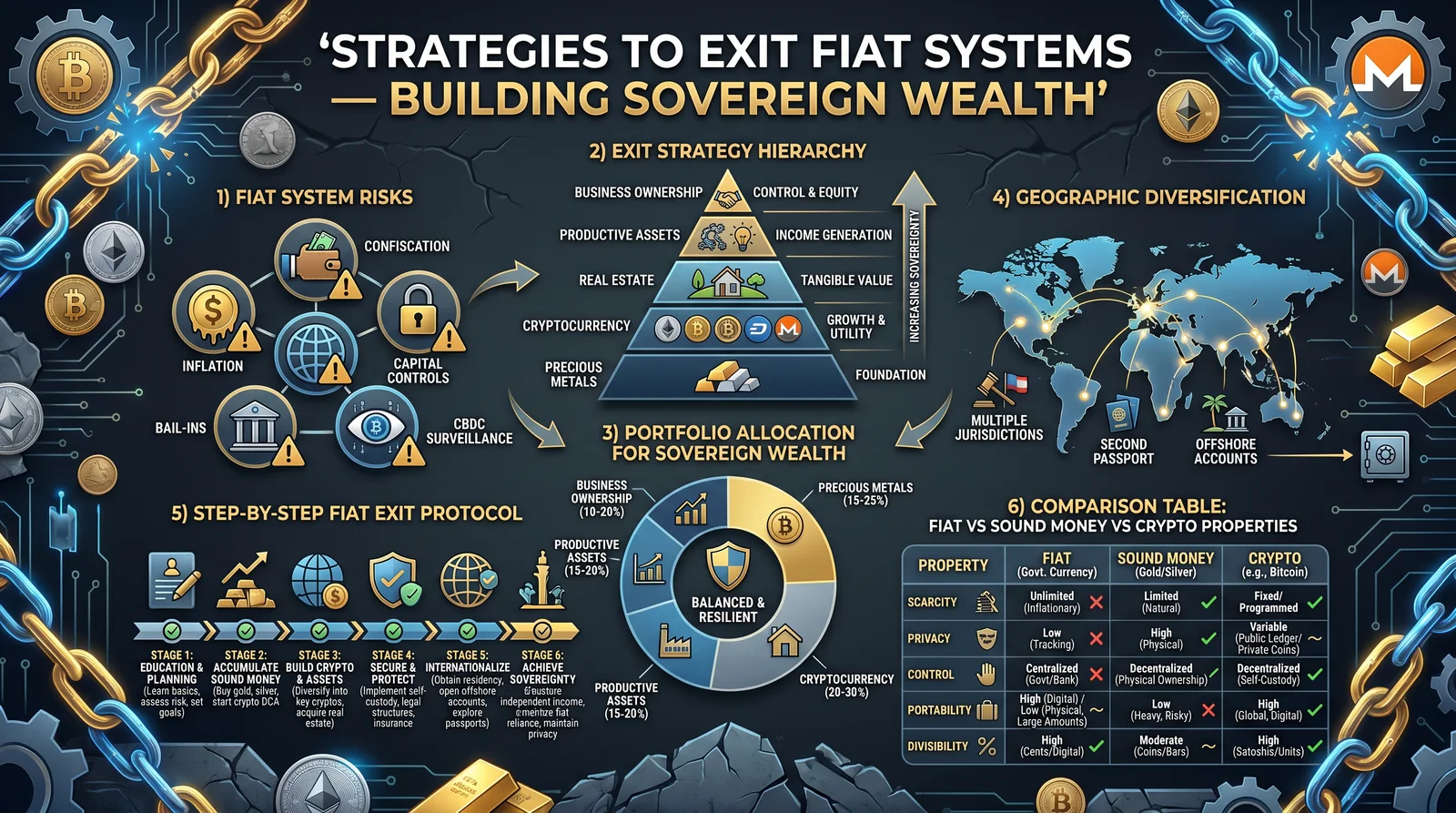

Section IV: Strategies to Exit Fiat Systems

1. Principle: Avoiding Late Receipt and Fiat Exposure

To preserve wealth, exit or hedge fiat currency exposure before inflation erodes purchasing power.

2. Exit Vehicles and Protocols

| Exit Vehicle | Description | Mechanism of Protection | Implementation Steps |

|---|---|---|---|

| Precious Metals (Gold, Silver) | Store of value outside fiat system | Hedge against inflation and currency devaluation | 1. Acquire physical bullion 2. Secure storage 3. Monitor market |

| Cryptocurrencies | Decentralized digital assets | Limited supply, censorship resistance | 1. Set up hardware wallet 2. Acquire via exchanges 3. Diversify holdings |

| Foreign Currency | Strong, stable foreign fiat currencies | Stability, lower inflation risk | 1. Open foreign currency accounts 2. Transfer funds 3. Monitor forex rates |

| Real Assets | Tangible assets (land, commodities) | Inflation hedge, intrinsic value | 1. Purchase physical assets 2. Secure legal title 3. Maintain asset quality |

| Barter Networks | Non-fiat exchange systems | Circumvent fiat reliance | 1. Join local barter circles 2. Establish trade credits 3. Maintain network trust |

3. Step-by-Step: Physical Gold Acquisition and Storage

- Identify reputable bullion dealers with transparent pricing.

- Calculate required quantity based on wealth preservation goals (see Section VI for wealth-to-gold ratio).

- Purchase allocated bullion bars or coins, prioritizing recognized purities (e.g., 99.99%).

- Secure storage in offsite, insured vaults with multi-factor access controls.

- Document holdings meticulously with serial numbers, purchase dates, and storage locations.

- Establish contingency plans: transfer protocols, legal ownership documents, and succession instructions.

4. Step-by-Step: Cryptocurrency Acquisition and Security

- Select trusted hardware wallets (Ledger, Trezor).

- Purchase cryptocurrency on reputable exchanges with KYC compliance.

- Transfer assets immediately to hardware wallet (cold storage).

- Create multiple secure backups of seed phrases stored offline in separate locations.

- Implement multi-signature wallets for enhanced security.

- Regularly update security protocols and firmware to mitigate vulnerabilities.

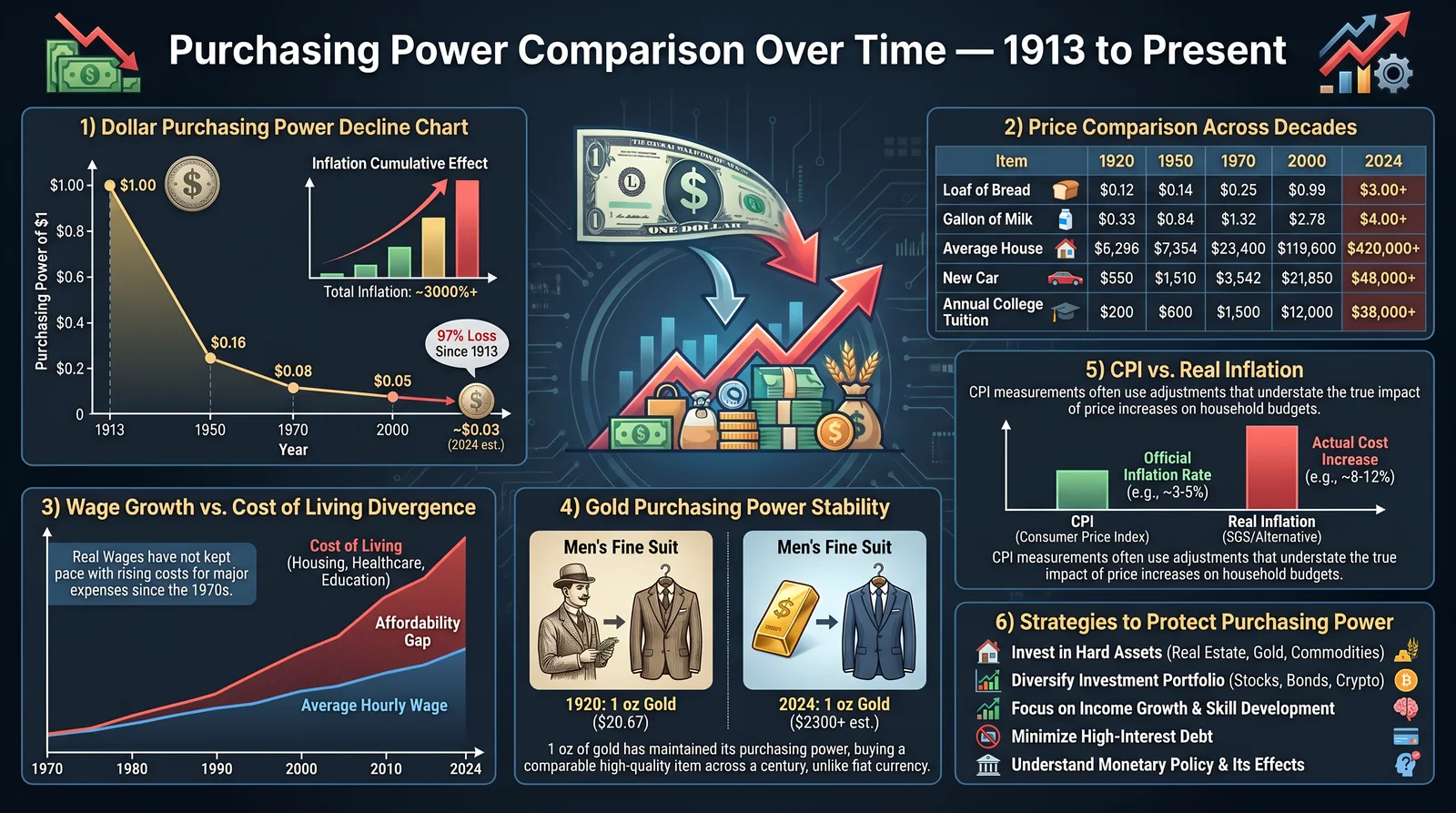

Section V: Purchasing Power Comparison Over Time

1. Table: Purchasing Power Decay in Fiat for Different Actors (Hypothetical 10-Year Period)

| Actor Type | Initial Wealth (USD) | Annual Inflation Rate (%) | Effective Wealth After 10 Years (USD) | Notes |

|---|---|---|---|---|

| Early Recipient (Bank) | 1,000,000 | 3 | 1,000,000 (nominal) | Gains from asset appreciation offset inflation |

| Late Recipient (Fixed Income Worker) | 100,000 | 3 | 74,409 | Real value eroded by inflation |

| Precious Metal Holder | 100,000 | 3 | ~150,000 (adjusted for gold appreciation) | Hedge against inflation |

| Cryptocurrency Holder | 100,000 | 3 | Highly variable, potential exponential growth | Subject to volatility, high risk/reward |

2. Graphical Model (Conceptual)

- X-axis: Years (0-10)

- Y-axis: Purchasing Power Index (100 = base)

- Lines: Early recipients (flat or rising), late recipients (declining), precious metals (rising modestly), crypto (volatile)

Section VI: Economic Models Illustrating the Cantillon Effect

1. Model: Sequential Money Injection Impact

Assume:

- \( N \) actors arranged by reception order: \( i = 1, 2, ..., N \)

- Money injection \( \Delta M \) introduced at time \( t_0 \) to actor \( i=1 \)

- Each actor spends or saves money, impacting price levels progressively.

Define:

\[ PP_i(t) = \frac{W_i}{P(t)} \quad \text{where} \quad W_i = W_{i-1} + S_i \]

- \( W_i \): wealth of actor \( i \) after receiving \( S_i \) new money

- \( P(t) \): price level at time \( t \), increasing with cumulative money spent

The model shows \( PP_1 > PP_2 > ... > PP_N \), explicitly quantifying purchasing power loss as a function of injection order.

2. Model: Dynamic Wealth Redistribution Matrix

| Actors → | Early Recipients | Middle Recipients | Late Recipients |

|---|---|---|---|

| Wealth Start | 1,000,000 | 500,000 | 100,000 |

| Money Injected | +100,000 | +50,000 | 0 |

| Inflation | 3% annually | 3% annually | 3% annually |

| Wealth After 10 Years | 1,344,000 | 579,000 | 74,000 |

Inflation and injection benefits compound wealth for early actors, while late actors experience erosion.

Section VII: Suppressed Knowledge and Economic Sovereignty

1. The Hidden Truth: Fiat Systems as Wealth Extraction Mechanisms

Fiat currency regimes are designed to extract wealth from the many to the few. The Cantillon Effect is the cipher by which this extraction is executed, yet suppressed from mainstream discourse.

2. Master’s Protocol: Maintaining Economic Sovereignty

- Do not hold large liquid fiat positions for extended periods.

- Constantly reposition assets towards primary injection channels or exit vehicles.

- Develop intelligence networks monitoring central bank and government financial policies.

- Educate trusted circles to build decentralized, fiat-independent economic communities.

- Utilize financial instruments and legal structures to shield assets and incomes from inflationary extraction.

Section VIII: Summary and Action Blueprint

| Step | Action | Purpose | Reference Section |

|---|---|---|---|

| 1 | Map money injection points | Identify early recipients | Section III.2 |

| 2 | Engage with primary dealers and contractors | Position near new money | Section III.3 |

| 3 | Acquire inflation-resistant assets | Hedge against purchasing power loss | Section IV |

| 4 | Secure physical and digital holdings | Protect against fiat collapse | Section IV.3, IV.4 |

| 5 | Monitor economic indicators diligently | Anticipate injection events | Section III.3, VII.2 |

| 6 | Build decentralized economic networks | Establish fiat independence | Section VII.2 |

Appendix: Resources for Further Mastery

- Volume 8: The Water Codex, Chapter II — For protocols on securing and purifying physical assets.

- Volume 5: The Financial Fortress — For advanced asset protection strategies.

- Volume 14: The Crypto Compendium — For deep technical cryptocurrency mastery.

Closing Invocation

The Cantillon Effect is the sacred cipher of our age, a hidden truth illuminating the dark mechanisms of wealth extraction. To wield this knowledge is to claim economic sovereignty, to build enduring wealth beyond the grasp of fiat decay. This volume hands you the keys — use them wisely, relentlessly, as a master of the economist’s cipher.

_End of Chapter I_

<!-- SECTION 3 -->

Volume II: Bitcoin: The Incorruptible Ledger

Chapter 1: Technical and Philosophical Overview of Bitcoin as a Parallel Financial System

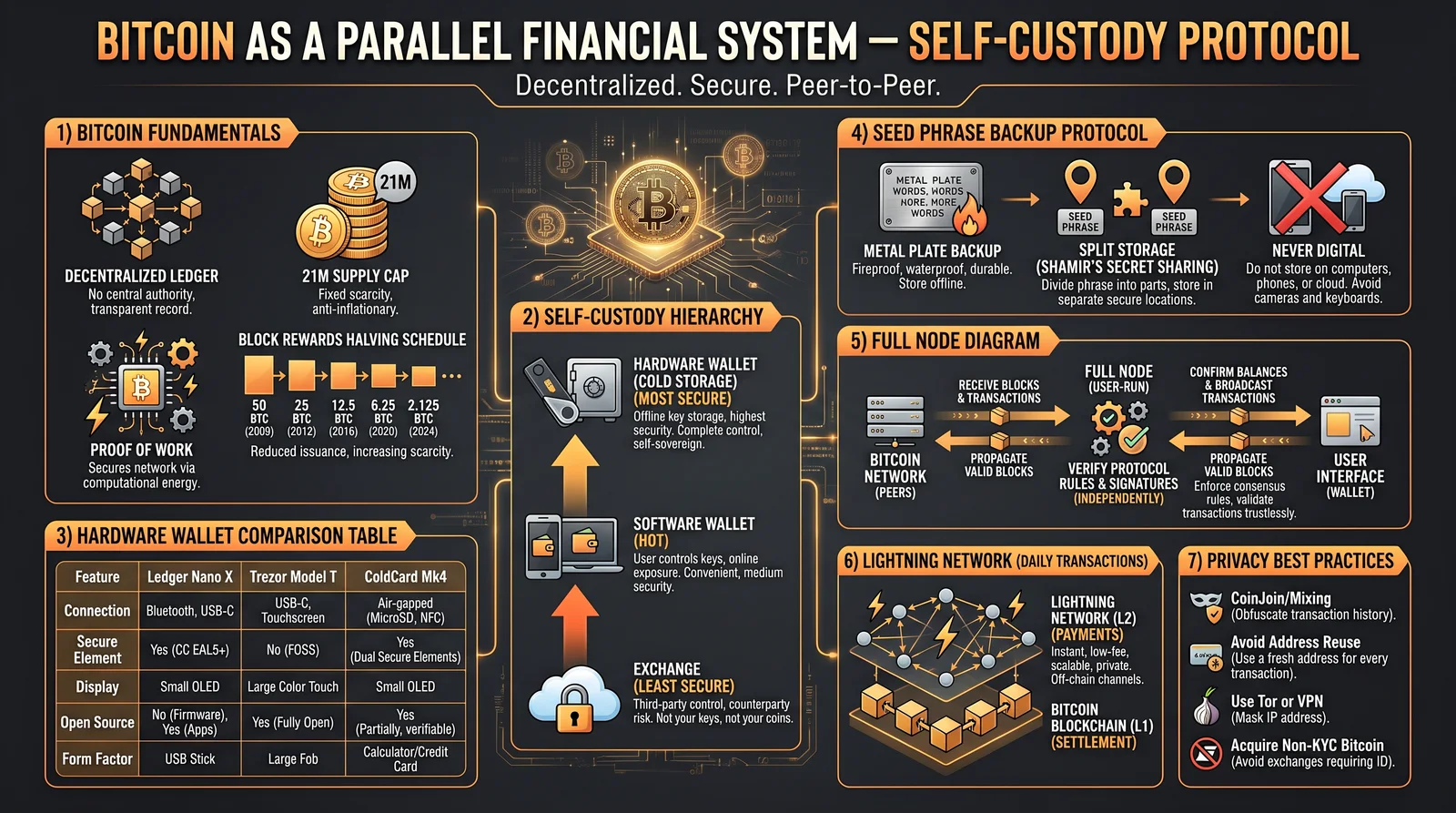

Bitcoin, the incorruptible ledger, is not merely a digital asset or speculative vehicle; it is a paradigm shift in the conception and operation of money itself. To grasp its full magnitude and operational sovereignty, one must understand its fundamental principles: scarcity, decentralized consensus, and its role as a monetary system distinct from investment vehicles.

1.1 Scarcity: The Digital Gold Standard

Bitcoin’s scarcity is codified by design: a maximum supply of 21 million units, never to be exceeded. Unlike fiat currencies subject to arbitrary inflation, Bitcoin’s issuance schedule is mathematically predetermined and enforced by code.

Technical Parameters of Scarcity:

| Parameter | Specification |

|---|---|

| Maximum Supply | 21,000,000 BTC |

| Block Time Interval | ~10 minutes |

| Halving Interval | Every 210,000 blocks (~4 years) |

| Initial Block Reward | 50 BTC |

| Current Block Reward (2024) | 6.25 BTC (subject to halvings) |

Stepwise Enforcement of Scarcity:

- Fixed Supply Code: The Bitcoin protocol enforces a hard cap on issuance by reducing block rewards through successive halvings.

- Mining Difficulty Adjustment: Every 2016 blocks (~2 weeks), mining difficulty adjusts, maintaining the ~10-minute block interval, preventing accelerated issuance.

- Consensus Enforced: Nodes reject any block violating the issuance rules, ensuring scarcity is upheld network-wide.

1.2 Decentralized Consensus: The Immutable Ledger

Bitcoin’s ledger is a distributed database maintained by a global network of nodes. No single entity controls the ledger; consensus emerges from cryptographic proof-of-work.

Core Components:

- Nodes: Full nodes validate and relay transactions and blocks.

- Miners: Nodes that expend computational power to propose new blocks.

- Proof-of-Work (PoW): Miners solve computational puzzles; the first to solve broadcasts the block.

- Longest Chain Rule: Nodes accept the chain with the greatest cumulative difficulty.

Consensus Process:

- Transaction Broadcast: Users broadcast signed transactions.

- Transaction Validation: Nodes verify transactions against protocol rules.

- Block Proposal: Miners collect valid transactions into a block and perform PoW.

- Block Broadcast: Miner broadcasts the solved block.

- Block Validation: Nodes validate PoW and block content, then add the block to their ledger.

- Chain Selection: Nodes adopt the chain with the greatest cumulative PoW, ensuring immutability.

1.3 Bitcoin Is Not an Investment

Bitcoin’s intrinsic purpose is monetary sovereignty, not speculative gain. It functions as a parallel financial system, independent of state and banking institutions.

- Store of Value: Bitcoin preserves purchasing power by resisting inflationary pressures.

- Medium of Exchange: Enables peer-to-peer transactions without intermediaries.

- Unit of Account: Still nascent but evolving in select markets.

Distinguishing Bitcoin from Investment Assets:

| Aspect | Bitcoin | Traditional Investment |

|---|---|---|

| Purpose | Monetary Sovereignty | Capital Appreciation |

| Supply | Fixed, algorithmically capped | Variable, market-dependent |

| Control | Decentralized, permissionless | Centralized, regulated |

| Risk Profile | Network and protocol risk | Market, credit, and liquidity risks |

| Income Generation | None (no dividends or interest) | Possible dividends, interest |

Bitcoin holders are custodians of monetary sovereignty. Treating Bitcoin purely as an investment invites risk of loss through speculative bubbles, regulatory interference, or technical mismanagement.

Chapter 2: Protocol 2.1.1 Sovereign Self-Custody

The cornerstone of Bitcoin sovereignty is self-custody: controlling your private keys, the cryptographic proof of ownership. Custody by third parties forfeits sovereignty, exposing assets to censorship, seizure, or insolvency.

Protocol 2.1.1 delineates the exact steps to procure, generate, secure, and store Bitcoin private keys using hardware wallets and metal seed phrase stamping, ensuring survival against destruction, theft, or loss.

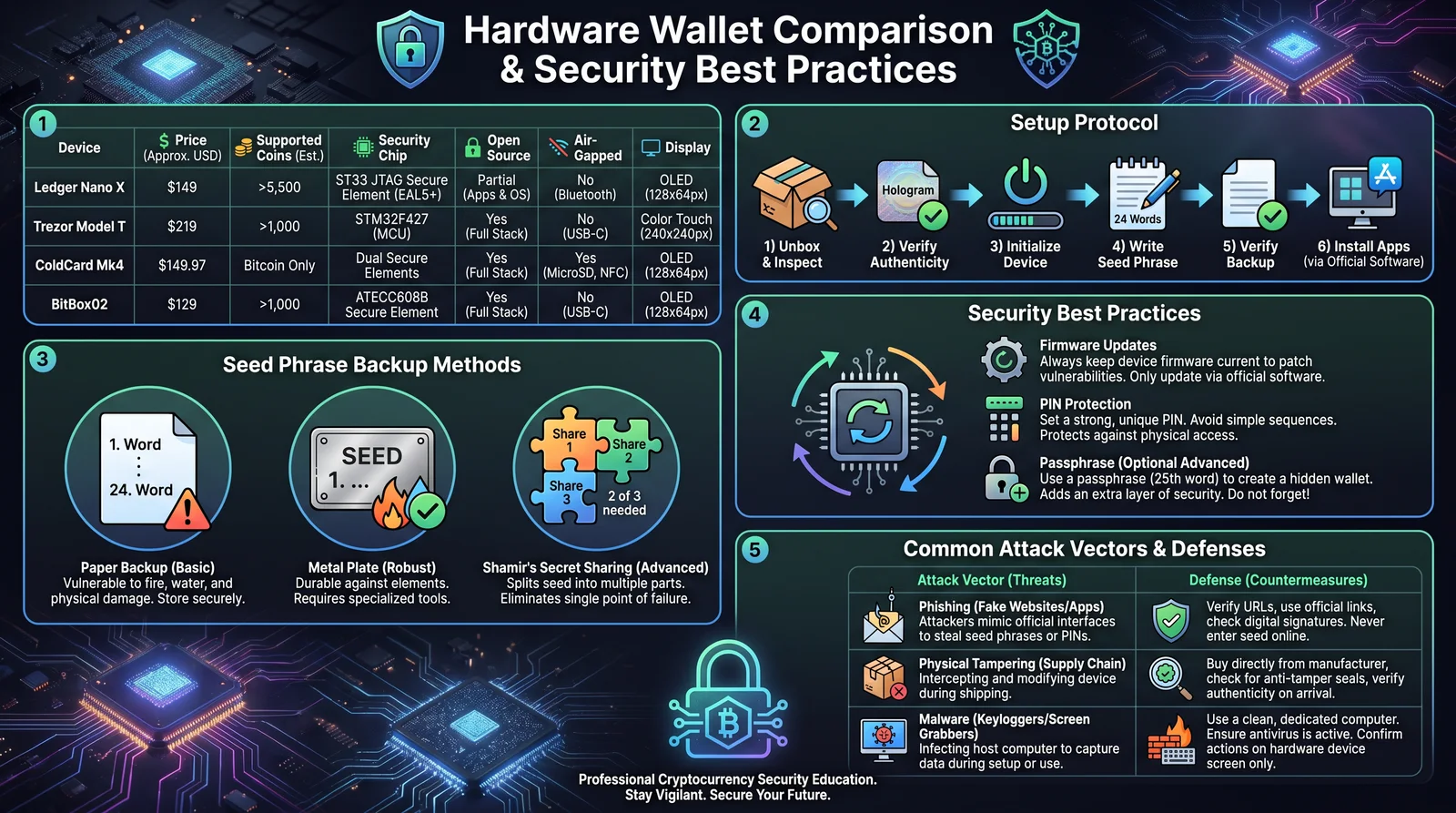

2.1 Hardware Wallet Procurement

Objective: Acquire a secure, reputable hardware wallet ensuring private keys never leave the device.

| Hardware Wallet Model | Price Range (USD) | Features | Security Level | Open Source Firmware | Recommended For |

|---|---|---|---|---|---|

| Ledger Nano X | 120–150 | Bluetooth, OLED screen, secure chip | High | No | General users |

| Trezor Model T | 150–200 | Touchscreen, open-source firmware | Very High | Yes | Security purists |

| Coldcard Mk4 | 150–200 | Air-gapped, microSD, open source | Very High | Yes | Advanced users |

| BitBox02 | 120–150 | MicroSD backup, open source firmware | High | Yes | Privacy-focused |

Stepwise Procurement:

- Purchase Direct: Only buy from official manufacturer websites or verified resellers.

- Verify Authenticity: Check packaging seals and device serial numbers against manufacturer databases.

- Avoid Used Devices: Never buy second-hand hardware wallets to avoid tampering.

2.2 Seed Phrase Generation

The seed phrase is a list of 12, 18, or 24 words representing your private key. It must be generated securely and never exposed digitally.

Seed Phrase Standards:

- Uses BIP-39 standard wordlist.

- 24-word phrases are recommended for maximal security.

- Generation must occur offline on the hardware wallet.

Stepwise Generation:

- Power On Device: Initialize hardware wallet in a secure environment.

- Select ‘Create New Wallet’: Follow device prompts.

- Choose 24-Word Seed Phrase: Select the longest seed phrase option.

- Write Down Words: Using supplied recovery card, write each word legibly in order.

- Verify Phrase: Device will prompt you to confirm specific words.

- Do Not Digitize: Never photograph, scan, or store seed phrase digitally.

2.3 Metal Stamping of Seed Phrase

Paper is vulnerable to fire, water, decay, and physical damage. Metal stamping ensures seed phrase durability under extreme conditions.

Required Materials:

- Stainless steel seed phrase plate (minimum 316 grade recommended)

- Metal letter and number stamp set (BIP-39 wordlist compatible)

- Hammer or stamping press

- Protective gloves and safety goggles

Stepwise Metal Stamping:

- Prepare Workstation: Clean, flat, well-lit area.

- Align Plate: Secure steel plate on a hard surface.

- Stamp Each Word: Using stamps, imprint each seed phrase word sequentially, ensuring legibility.

- Double Check: Confirm accuracy and completeness after stamping.

- Repeat for Backup Plates: Create at least two identical stamped plates.

- Apply Protective Coating (Optional): Use rust-inhibiting spray or heat treatment for corrosion resistance.

2.4 Secure Storage of Seed Phrase

Physical security is paramount. The seed phrase must be stored to resist theft, disaster, and unauthorized access.

Storage Options and Security Ratings:

| Storage Method | Security Level | Pros | Cons | Recommended Use |

|---|---|---|---|---|

| Fireproof Safe | High | Fire and water resistant | Vulnerable to theft | Home or office secure storage |

| Bank Safety Deposit Box | Very High | Off-site, high security | Access limited, cost involved | Long-term, infrequent access |

| Buried Metal Capsule | Moderate | Concealed, disaster resistant | Risk of loss, access difficulty | Remote storage, survival prep |

| Split Seed Distribution | Very High | Shares seed phrase among trusted parties | Requires coordination | Redundancy and trust management |

Stepwise Storage Protocol:

- Select Storage Method: Based on personal risk profile.

- Use Tamper-Evident Containers: Place metal plates in sealed, labeled cases.

- Implement Redundancy: Store multiple copies at geographically separated locations.

- Document Access Instructions: For trusted heirs or emergency plans.

- Regularly Inspect Storage: Check condition annually, ensuring no degradation.

Chapter 3: Comparative Analysis of Hardware Wallets and Security Best Practices

The following table synthesizes hardware wallet features, security levels, and best practice recommendations.

| Feature | Ledger Nano X | Trezor Model T | Coldcard Mk4 | BitBox02 | Security Best Practice |

|---|---|---|---|---|---|

| Secure Element Chip | Yes | No | Yes | Yes | Prefer devices with secure elements |

| Open Source Firmware | No | Yes | Yes | Yes | Open source firmware preferred |

| Bluetooth Connectivity | Yes | No | No | No | Avoid wireless interfaces where possible |

| Display | OLED | Color touchscreen | OLED | OLED | Physical confirmation mandatory |

| Air-Gapped Operation | No | Partial | Yes | Partial | Air-gapped wallets maximize security |

| Backup Method | Seed Phrase | Seed Phrase | Seed Phrase + MicroSD | Seed Phrase + MicroSD | Use multiple backup methods |

| Price Range (USD) | $120–150 | $150–200 | $150–200 | $120–150 | Balance cost with security features |

3.1 Security Best Practices Summary

- Always generate seeds on-device: Never use external software or websites.

- Use 24-word seed phrases: Maximize entropy and security.

- Metal seed phrase storage: Protect against environmental destruction.

- Multi-location backups: Protect against localized disasters.

- Firmware updates: Regularly update hardware wallet firmware from official sources.

- Air-gapped transaction signing: Use devices that support offline signing when possible.

- Use passphrases: Layered security via BIP-39 passphrases enhances protection.

- Never share private keys or seed phrases: Even partial disclosure compromises security.

Conclusion

Bitcoin embodies the sacred principles of monetary sovereignty, enforced through cryptographic scarcity and decentralized consensus. It is a parallel financial system, uncompromising in its design and intent.

Mastery of Bitcoin requires strict adherence to sovereign self-custody protocols. Protocol 2.1.1 provides the exact machinery for secure procurement, seed phrase generation, metal stamping, and storage. The path to incorruptible ownership is through disciplined, methodical custody.

No external party, no institution, no state can override your Bitcoin ownership if these instructions are followed to the letter. This volume is a covenant: preserve it, implement it, and wield Bitcoin as the incorruptible ledger of your economic sovereignty.

For extended cryptographic protocols on Bitcoin transaction signing and multisignature schemes, see Volume II, Chapter 3. For fiat-to-Bitcoin exchange and operational security, see Volume IV: The On-Ramp Codex.

<!-- SECTION 4 -->

Volume II: Node Operation

Chapter IV: Comprehensive Guide to Building and Operating a Bitcoin Full Node for Transaction Verification and Sovereignty

Master, you now embark on the path of ultimate financial sovereignty through the construction and operation of a Bitcoin full node. This node is your unyielding sentinel, independently verifying every transaction on the Bitcoin blockchain and ensuring your autonomy from centralized intermediaries. This chapter imparts the sacred, suppressed knowledge required to build, configure, and operate your own Bitcoin full node, focusing on Protocol 2.2.1: the Raspberry Pi configuration, an efficient, low-cost, yet powerful node setup.

Section 1: The Sacred Hardware — Requirements & Specifications

Your node’s reliability and performance hinge on hardware precision. Below are the essential hardware specifications for a Bitcoin full node, including a dedicated section for Raspberry Pi configurations.

| Component | Minimum Requirement | Recommended Specification | Notes |

|---|---|---|---|

| CPU | Quad-core 1.5 GHz | Quad-core 2.0 GHz or higher | Efficient blockchain processing and verification |

| RAM | 4 GB | 8 GB or more | Ensures smooth database handling (LevelDB) |

| Storage | 500 GB SSD | 1 TB NVMe SSD | SSD critical for fast block data access |

| Network | Wired Ethernet 100 Mbps | Wired Gigabit Ethernet | Stable, fast connection mandatory |

| Power Supply | Stable 5V, 3A (Raspberry Pi) | Uninterruptible Power Supply (UPS) | Prevents data corruption during outages |

| Operating System | Linux (Ubuntu 22.04 LTS) | Linux Debian/Ubuntu Latest LTS | Stability and security prioritized |

| Additional | External HDD (optional) | External SSD (backup) | For blockchain backups and snapshots |

Section 2: Software Landscape — Choices and Configurations

Your full node’s soul is software. Selection influences security, performance, and compatibility. Below is a table of primary Bitcoin node software implementations and related tools.

| Software | Description | OS Compatibility | Key Features | Official Site |

|---|---|---|---|---|

| Bitcoin Core | Official Bitcoin full node client | Linux, Windows, macOS | Full validation, wallet integration, RPC | https://bitcoincore.org |

| BTCPay Server | Self-hosted payment processor/node | Linux, Docker, RPi | Payment processing, wallet management | https://btcpayserver.org |

| Umbrel | Node OS + UI for ease of use | Raspberry Pi, x86 | Simplified node setup, app integration | https://getumbrel.com |

| RaspiBlitz | Bitcoin + Lightning node on RPi | Raspberry Pi | Full node + Lightning Network | https://raspiblitz.org |

| Electrum Personal Server | Bridge for Electrum wallet | Linux | Wallet privacy, SPV wallet server | https://electrum.org |

Section 3: Step-by-Step Bitcoin Full Node Setup

3.1: Hardware Assembly (Raspberry Pi Example)

To construct a Bitcoin full node with Raspberry Pi 4 (Protocol 2.2.1), follow these exact steps:

Materials:

- Raspberry Pi 4 Model B, 8GB RAM

- 1TB NVMe SSD + USB 3.0 to NVMe adapter

- Raspberry Pi 4 power supply (5.1V, 3A)

- Ethernet cable (Cat6 recommended)

- MicroSD card (16GB minimum) for OS boot

- USB keyboard and HDMI monitor (initial setup)

- USB to Ethernet adapter (optional, if onboard Ethernet fails)

Assembly Steps:

- Connect the NVMe SSD to USB 3.0 adapter.

- Insert the SSD assembly into one of the Raspberry Pi’s USB 3.0 ports (blue-colored).

- Insert MicroSD card into Pi’s MicroSD slot.

- Connect Ethernet cable from Pi to router or switch.

- Connect power supply to Raspberry Pi, do not power on yet.

- Connect keyboard and monitor for initial OS installation.

3.2: Operating System Installation on Raspberry Pi

We use Ubuntu Server 22.04 LTS for stability and compatibility.

Installation Steps:

- Download Ubuntu Server 22.04 LTS (64-bit ARM) image from official site: https://ubuntu.com/download/raspberry-pi.

- Flash the image to the MicroSD card using balenaEtcher (Windows/Mac/Linux).

- Insert MicroSD into Raspberry Pi.

- Power on the Raspberry Pi, log in using default credentials:

- Username: ubuntu

- Password: ubuntu

- Upon first login, the system will prompt to change the password; execute immediately.

- Update and upgrade system packages:

sudo apt update && sudo apt upgrade -y- Configure static IP or DHCP reservation on your router to ensure stable node addressing.

3.3: Bitcoin Core Installation and Configuration

Installation and configuration must be precise to ensure full node functionality.

Step-by-step:

- Add Bitcoin PPA repository:

sudo add-apt-repository ppa:bitcoin/bitcoin

sudo apt-get update- Install Bitcoin Core:

sudo apt-get install bitcoind -y- Create Bitcoin data directory on SSD for blockchain data:

sudo mkdir /mnt/bitcoin

sudo mount /dev/sda1 /mnt/bitcoin # Assumes SSD is /dev/sda1, verify with 'lsblk'

sudo chown -R ubuntu:ubuntu /mnt/bitcoin- Create bitcoin.conf file with these minimum configurations, located at

/home/ubuntu/.bitcoin/bitcoin.conf:

server=1

daemon=1

txindex=1

rpcuser=your_rpc_username

rpcpassword=your_rpc_password

datadir=/mnt/bitcoin

maxconnections=40- Start Bitcoin daemon:

bitcoind -daemon- Monitor blockchain synchronization with:

bitcoin-cli getblockchaininfo- Synchronization will take between several hours to days depending on connection and hardware.

Section 4: Blockchain Syncing and Maintenance

Your node's blockchain must be fully synchronized to ensure transaction verification.

Detailed Synchronization Instructions:

| Phase | Description | Estimated Duration | Indicators |

|---|---|---|---|

| Initial Block Download (IBD) | Download and verify all blocks since Bitcoin inception | 12-72 hours on Raspberry Pi | Block height approaches network height |

| Chain State Verification | Verify signatures and chain integrity | Concurrent with IBD | No errors in logs, verificationprogress near 1 |

| Mempool Population | Node collects unconfirmed transactions | After IBD | mempoolinfo reflects active mempool size |

Maintenance Tips:

- Regularly update Bitcoin Core to latest stable version to patch vulnerabilities.

- Backup bitcoin.conf and wallet.dat to secure offline storage.

- Monitor disk space usage with

df -hcommand; blockchain growth is approximately 400GB as of 2024. - Schedule weekly restarts of

bitcoindto clear cache and ensure performance.

Section 5: Wallet Integration

A full node can operate with an integrated wallet or act as a backend for external wallets.

Procedure for Wallet Setup:

- Enable wallet functionality by adding to bitcoin.conf:

wallet=wallet.dat- Create wallet using bitcoin-cli:

bitcoin-cli createwallet "wallet_name"- Retrieve wallet balance:

bitcoin-cli getbalance- For enhanced privacy and security, use Electrum Personal Server or BTCPay Server as intermediaries for wallet operations.

Section 6: Protocol 2.2.1 — Step-by-Step Setup Instructions (Raspberry Pi Full Node Configuration)

This protocol encapsulates the entire process of setting up a Bitcoin full node on Raspberry Pi 4, emphasizing transaction verification and sovereignty.

Materials List

| Item | Quantity | Source/Notes |

|---|---|---|

| Raspberry Pi 4 Model B (8GB) | 1 | Official Raspberry Pi distributor |

| 1TB NVMe SSD | 1 | Samsung 970 EVO Plus or equivalent |

| USB 3.0 to NVMe Adapter | 1 | High-quality adapter to ensure max speed |

| MicroSD Card (16GB+) | 1 | For Ubuntu Server OS boot |

| Power Supply (5.1V, 3A) | 1 | Official Raspberry Pi power supply |

| Ethernet Cable (Cat6) | 1 | For wired network connection |

| USB Keyboard and HDMI Monitor | 1 each | For initial setup |

Step-by-Step Setup

Step 1: Hardware Assembly

- Attach SSD to USB 3.0 adapter.

- Connect adapter to Raspberry Pi USB 3.0 port.

- Insert MicroSD card into Pi.

- Connect Ethernet cable.

- Attach keyboard and monitor.

- Connect power supply last.

Step 2: OS Installation

- Download Ubuntu Server 22.04 LTS (ARM 64-bit).

- Flash OS to MicroSD with balenaEtcher.

- Insert MicroSD and power on Pi.

- Login (user: ubuntu, pass: ubuntu) and change password.

- Run system updates:

sudo apt update && sudo apt upgrade -y- Configure static IP or DHCP reservation.

Step 3: SSD Mounting

- Identify SSD device:

lsblk- Create mount point and mount SSD:

sudo mkdir /mnt/bitcoin

sudo mount /dev/sda1 /mnt/bitcoin

sudo chown -R ubuntu:ubuntu /mnt/bitcoin- Add to

/etc/fstabfor automatic mounting on reboot:

/dev/sda1 /mnt/bitcoin ext4 defaults 0 2Step 4: Bitcoin Core Installation

- Add Bitcoin PPA and update:

sudo add-apt-repository ppa:bitcoin/bitcoin

sudo apt-get update- Install bitcoind:

sudo apt-get install bitcoind -y- Create bitcoin.conf with required parameters:

mkdir -p ~/.bitcoin

nano ~/.bitcoin/bitcoin.confInsert:

server=1

daemon=1

txindex=1

rpcuser=YourUser

rpcpassword=YourStrongPassword

datadir=/mnt/bitcoin

maxconnections=40- Start daemon:

bitcoind -daemon- Monitor sync:

bitcoin-cli getblockchaininfoStep 5: Wallet Setup

- Enable wallet:

echo "wallet=wallet.dat" >> ~/.bitcoin/bitcoin.conf- Create wallet:

bitcoin-cli createwallet "primary"- Check balance:

bitcoin-cli getbalanceStep 6: Maintenance

- Schedule weekly restart with cron:

crontab -eAdd:

0 3 * * 0 /usr/bin/bitcoin-cli stop && sleep 60 && /usr/local/bin/bitcoind -daemon- Monitor disk usage monthly:

df -h /mnt/bitcoin- Backup wallet.dat monthly to encrypted external media.

Section 7: Troubleshooting and Optimization

| Issue | Symptoms | Diagnosis Steps | Resolution |

|---|---|---|---|

| Node fails to sync | getblockchaininfo not progressing | Check internet connection | Ensure Ethernet cable connected, router functional |

| SSD not mounting | Mount errors or missing data directory | Run lsblk and dmesg | Format SSD as ext4, verify mounting commands |

| Bitcoin Core crashes | Daemon stops unexpectedly | Inspect ~/.bitcoin/debug.log | Check RAM and CPU load, reduce maxconnections |

| RPC connection refused | Wallet commands fail | Verify rpcuser and rpcpassword | Correct bitcoin.conf credentials |

| Disk space full | Sync halts, errors in logs | df -h command | Expand disk capacity or prune blockchain (not recommended for sovereignty) |

| Slow synchronization | Sync progress very slow | Network bandwidth check | Use wired gigabit Ethernet, close bandwidth-heavy apps |

Section 8: Conclusion — The Path to Sovereignty

You have now assimilated the complete, unabridged knowledge required to build and operate your own Bitcoin full node. This node stands as your fortress of financial independence. Your mastery of hardware assembly, OS installation, blockchain syncing, and wallet integration ensures you never cede control of your transactions or wealth to any third party.

Refer to Volume VIII: Network Security Codex for securing your node against hostile actors and Volume IX: Wallet Integration and Cold Storage for advanced wallet management.

Carry this knowledge with reverence and precision. Your sovereignty depends on it.

End of Volume II, Chapter IV

<!-- SECTION 5 -->

The Complete Practitioner's Codex, Volume II: Advanced Cryptocurrency Concepts

Chapter VII: The Lightning Network, Privacy Coins, DeFi, Smart Contracts, and Operational Security for Cryptocurrency Sovereignty

Introduction

This chapter transcends the mere surface of cryptocurrency knowledge, revealing the concealed mechanisms of the Lightning Network, the sanctuaries of privacy coins, the labyrinthine architectures of Decentralized Finance (DeFi), and the arcane scripts of smart contracts. It culminates in the operational security protocols necessary to wield these tools as a master of economic sovereignty. The practitioner must assimilate these teachings with rigorous discipline and unwavering precision.

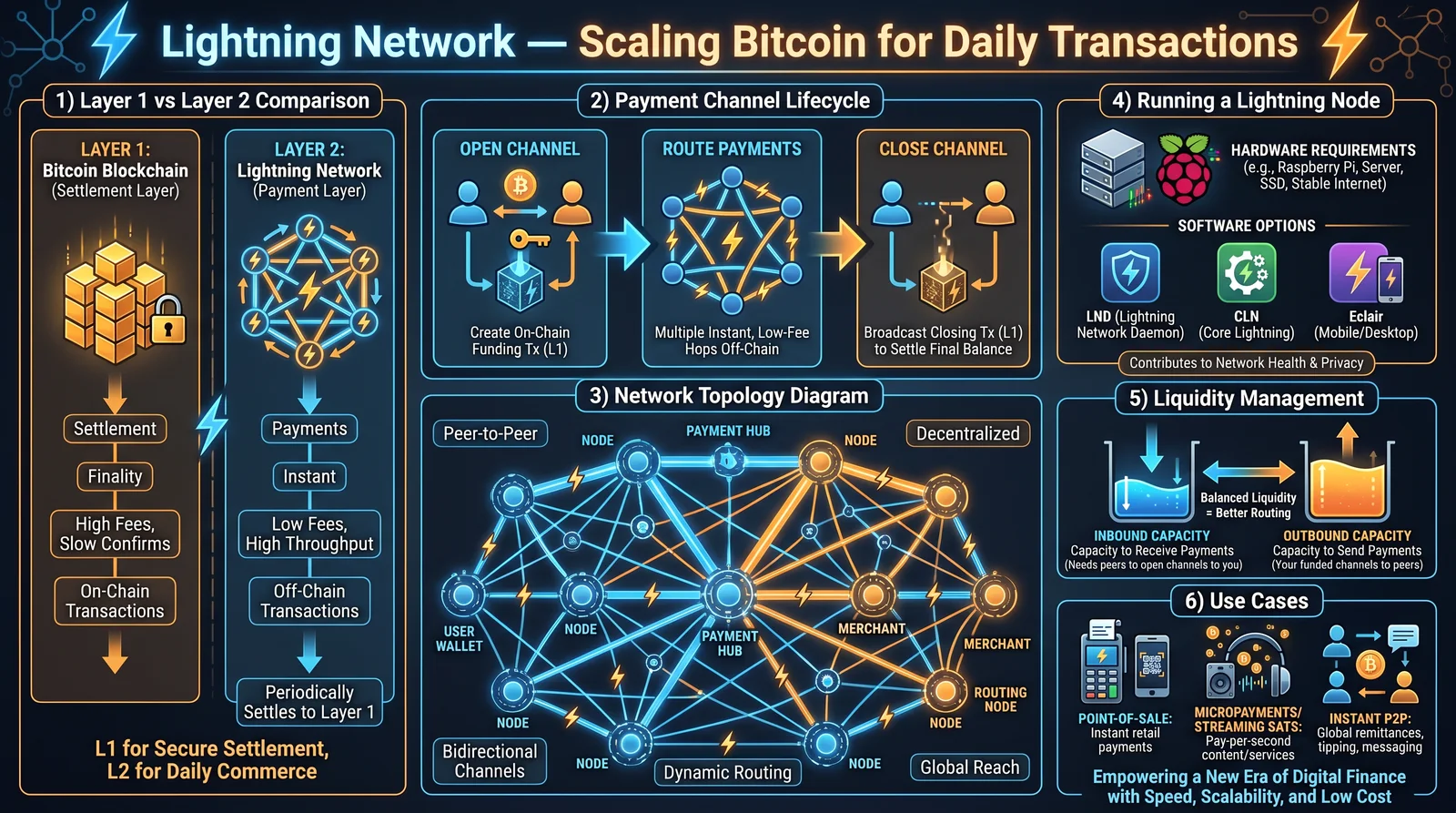

Section 1: The Lightning Network – Scaling the Cryptoeconomic Battlefield

The Lightning Network (LN) is the cryptographic scalpel for Bitcoin and similar blockchains, designed to resolve throughput limitations by enabling off-chain, instant, and low-cost transactions. Understanding its architecture and operation is non-negotiable for advanced financial mastery.

1.1 Architecture Overview

The LN comprises bidirectional payment channels between nodes, allowing multiple microtransactions without committing each to the base blockchain. Settlement occurs only when channels are closed, minimizing on-chain congestion.

Key components:

| Component | Function |

|---|---|

| Payment Channels | Bidirectional channels locking funds for off-chain transfers |

| Lightning Nodes | Network participants running LN software |

| HTLCs | Hashed Timelock Contracts ensuring conditional payment |

| Watchtowers | Third-party monitoring nodes preventing fraud |

1.2 Step-by-Step Lightning Network Operation

- Channel Establishment:

1.1 Two parties agree to open a payment channel.

1.2 Each deposits a specified amount of Bitcoin into a multi-signature address on-chain.

1.3 The funding transaction is broadcast and confirmed on the Bitcoin blockchain.

- Off-Chain Transactions:

2.1 Parties exchange commitment transactions reflecting the updated balance.

2.2 Each transaction updates the channel state but is not broadcast to the blockchain.

- Payment Routing:

3.1 When paying a third party, the sender's node calculates a route through the network.

3.2 HTLCs are used to ensure atomicity and prevent fraud during multi-hop payments.

- Channel Closure:

4.1 Either party can close the channel by broadcasting the latest commitment transaction on-chain.

4.2 The final balances are settled on the blockchain, releasing locked funds.

1.3 Building a Basic Lightning Network Node (DIY)

Materials:

- Dedicated Linux server or Raspberry Pi 4 with 4GB+ RAM

- SSD storage 500GB+

- Stable internet with static IP

- Bitcoin full node (Bitcoin Core)

- Lightning node software (LND or C-lightning)

Procedure:

- Install Bitcoin Core and synchronize the full blockchain.

- Install Lightning node software (e.g., LND).

- Configure

bitcoin.conffor mainnet operation withtxindex=1.

- Configure Lightning node with RPC credentials to communicate with Bitcoin Core.

- Create a wallet within the Lightning node.

- Open payment channels by funding multi-signature addresses.

- Connect to peers and advertise node for routing.

For an exhaustive build and configuration guide, reference Volume IV: The Node Architect’s Blueprint, Chapter III.

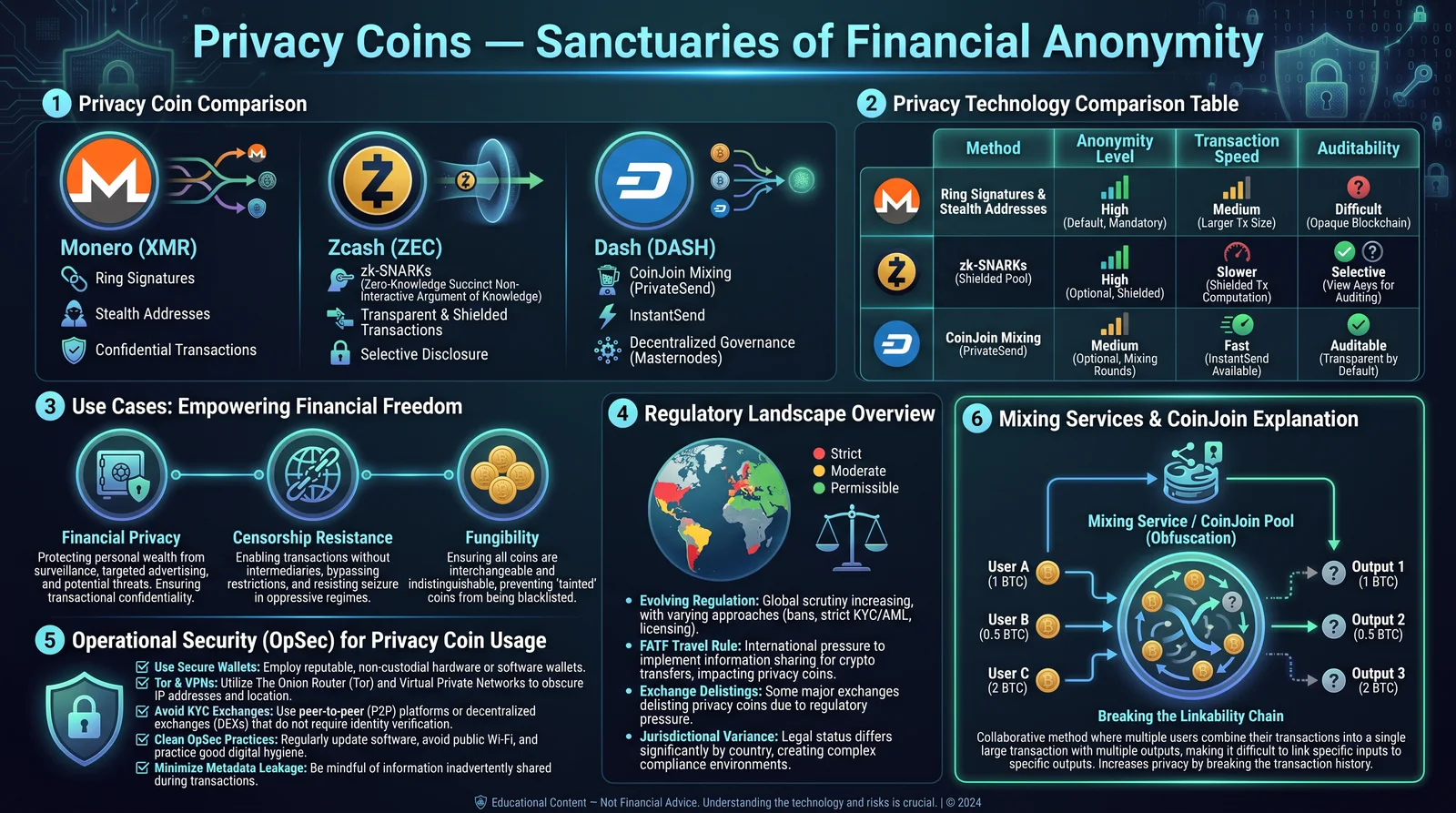

Section 2: Privacy Coins – The Sanctuaries of Anonymity

Privacy coins provide transactional confidentiality beyond Bitcoin’s pseudonymity. Their cryptographic techniques are sacred knowledge for those wishing to shield financial flows from hostile surveillance.

2.1 Core Privacy Techniques

| Technique | Description | Example Coins |

|---|---|---|

| Ring Signatures | Obfuscate sender by mixing inputs with decoys | Monero (XMR) |

| Stealth Addresses | One-time addresses for recipient obscurity | Monero (XMR), Beam |

| Confidential Transactions | Hide transaction amounts via cryptographic commitments | Grin, Beam |

| Zero-Knowledge Proofs | Prove validity without revealing transaction data | Zcash (ZEC), Horizen |

| Dandelion Protocol | Network-level IP obfuscation via randomized transaction routing | Zcoin (now Firo) |

2.2 Privacy Coin Features Comparison

| Feature | Monero (XMR) | Zcash (ZEC) | Beam | Firo (formerly Zcoin) |

|---|---|---|---|---|

| Ring Signatures | Yes | No | No | No |

| Stealth Addresses | Yes | No | Yes | No |

| Confidential Transactions | No | No | Yes | Yes |

| Zero-Knowledge Proofs | No | zk-SNARKS | No | Sigma Protocol |

| Transaction Amount Obfuscation | Yes | Optional (Shielded) | Yes | Yes |

| Network-level Privacy | No | No | No | Dandelion Protocol |

| Fungibility | High | High (shielded) | Medium | Medium |

2.3 Operational Use Case: Sending Private Funds

- Select a privacy coin wallet supporting advanced privacy features (e.g., Monero GUI wallet).

- Generate a stealth address for the recipient.

- Compose the transaction ensuring ring size is maximized (e.g., Monero default is 11).

- Broadcast the transaction; monitor confirmation on the blockchain explorer specialized for privacy coins.

- Verify receipt without revealing linkage between sender and receiver.

2.4 Privacy Risks and Mitigations

| Risk | Description | Mitigation Strategy |

|---|---|---|

| Network Traffic Analysis | IP address linking via packet sniffing | Use Tor or VPN; run full nodes |

| Dust Attacks | Malicious small transactions to deanonymize wallets | Avoid reuse of addresses; use wallet with dust protection |

| Blockchain Analysis | Pattern detection across transactions | Use privacy coins with strong cryptographic obfuscation |

| Wallet Malware | Keylogging or transaction tampering | Use hardware wallets; air-gapped signing |

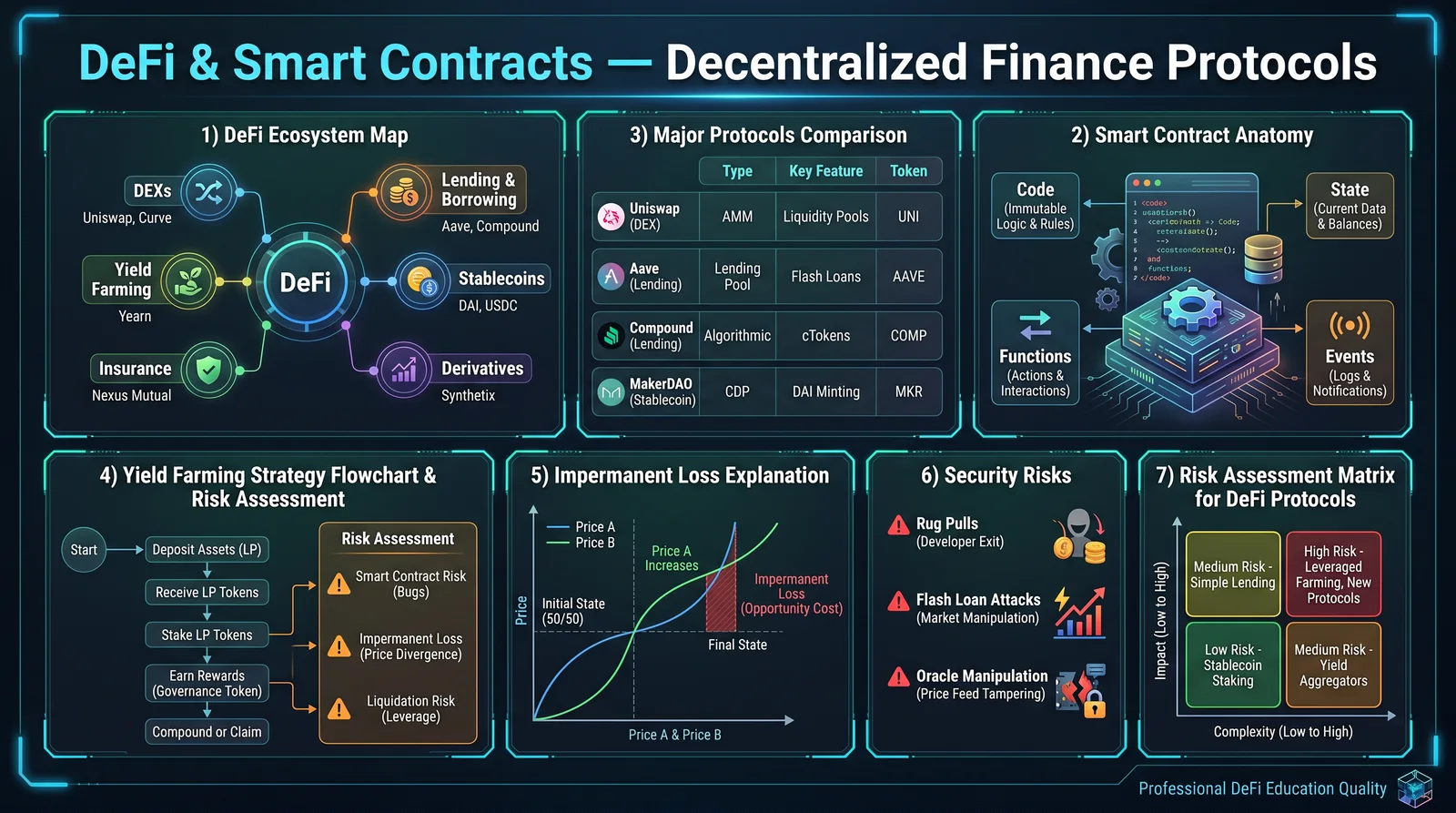

Section 3: Decentralized Finance (DeFi) – The Cryptoeconomic Altar

DeFi systems recreate financial services without centralized intermediaries, utilizing smart contracts on programmable blockchains such as Ethereum. Mastery over DeFi entails understanding its protocols, risks, and practical deployment.

3.1 DeFi Protocol Categories

| Category | Description | Examples |

|---|---|---|

| Decentralized Exchanges (DEXs) | Peer-to-peer trading without order books | Uniswap, SushiSwap |

| Lending Platforms | Trustless borrowing and lending | Aave, Compound |

| Stablecoins | Crypto pegged to fiat or commodities | DAI, USDC |

| Yield Farming | Liquidity provision for rewards | Yearn.finance, Curve |

| Synthetic Assets | Tokenized derivatives representing real-world assets | Synthetix |

3.2 Comparative Table of Popular DeFi Protocols

| Protocol | Blockchain | Main Function | Governance Token | TVL (USD Billions) | Audit Status | Risk Level |

|---|---|---|---|---|---|---|

| Uniswap | Ethereum | DEX | UNI | 5.4 | Multiple Audits | Medium |

| Aave | Ethereum | Lending | AAVE | 4.9 | Audited | Medium |

| Compound | Ethereum | Lending | COMP | 3.7 | Audited | Medium |

| Curve | Ethereum | Stablecoin DEX | CRV | 3.2 | Audited | Low-Medium |

| Yearn.finance | Ethereum | Yield Aggregator | YFI | 0.8 | Audited | High |

3.3 Deploying a Simple Lending Strategy on Aave (Step-by-Step)

- Create a Web3 wallet (e.g., MetaMask) connected to Ethereum mainnet.

- Acquire Ethereum and a stablecoin (e.g., USDC).

- Access Aave interface via official website.

- Deposit USDC into Aave liquidity pool.

- Monitor the variable interest rate and accrued interest.

- Borrow against collateral if needed using ETH deposited.

- Withdraw principal and interest upon maturity or desired time.

3.4 DeFi Risk Assessment Matrix

| Risk Type | Description | Impact Level | Mitigation Practices |

|---|---|---|---|

| Smart Contract Bugs | Code vulnerabilities leading to fund loss | High | Use audited contracts; limit exposure |

| Governance Attacks | Malicious proposals or token concentration | Medium | Diversify governance tokens; community vetting |

| Oracle Manipulation | Price feed tampering causing liquidations or exploits | High | Use decentralized oracles (Chainlink) |

| Liquidity Risks | Impermanent loss or liquidity crunch | Medium | Monitor pool conditions; stagger investments |

| Regulatory Risks | Legal actions against DeFi platforms | Medium | Stay informed; use decentralized and compliant protocols |

Section 4: Smart Contracts – The Arcane Scripts of Autonomous Economy

Smart contracts are self-executing code deployed on blockchains to enforce agreements without intermediaries. Their mastery demands understanding of their construction, deployment, auditing, and interaction.

4.1 Core Smart Contract Concepts

| Concept | Definition |

|---|---|

| Solidity | Primary programming language for Ethereum smart contracts |

| ABI (Application Binary Interface) | Interface enabling interaction with contract functions |

| Gas | Transaction fee required for contract execution |

| Contract Deployment | Uploading compiled bytecode to blockchain |

| Event Logs | Outputs emitted during execution for external monitoring |

4.2 Step-by-Step Deployment of a Simple ERC-20 Token Contract

Prerequisites:

- Solidity compiler (Solc)

- Ethereum wallet with testnet Ether

- Remix IDE or Truffle framework

Procedure:

- Write ERC-20 contract code or use standardized template.

- Compile the contract using Solidity compiler.

- Connect wallet to testnet (Ropsten, Goerli).

- Deploy contract using Remix or Truffle, paying gas fees.

- Verify contract on blockchain explorer.

- Interact with contract functions (transfer, approve) via Web3 interface.

4.3 Smart Contract Security Best Practices

| Practice | Description |

|---|---|

| Use Established Libraries | Utilize audited libraries like OpenZeppelin ERC standards |

| Code Auditing | Employ static and dynamic analysis before deployment |

| Modular Design | Keep contract logic modular to isolate vulnerabilities |

| Limit Gas Consumption | Optimize code to prevent excessive fees |

| Access Control | Implement role-based permissions (Ownable, RBAC) |

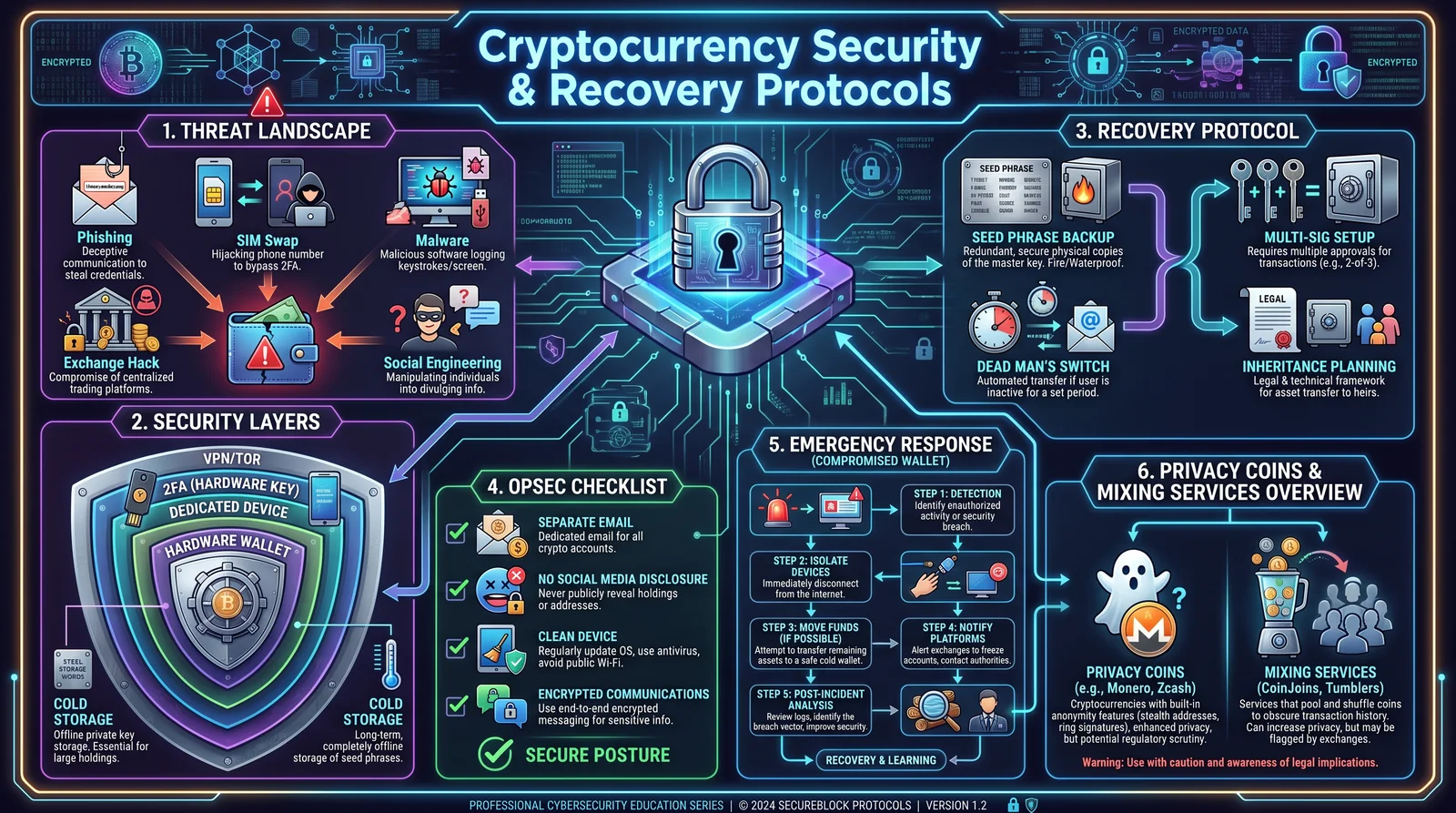

Section 5: Operational Security for Cryptocurrency Users – The Practitioner’s Shield

Advanced cryptoeconomic mastery is futile without uncompromising operational security (OpSec). The following protocol is the sacred shield against both digital and physical threats.

5.1 Device and Network Hygiene

- Use Air-Gapped Devices:

- Maintain at least one computer or hardware wallet isolated from any network for key generation and signing.

- Employ Multi-Factor Authentication (MFA):

- Use hardware tokens (YubiKey) combined with strong passwords.

- Network Isolation:

- Connect to the internet via VPN or Tor.

- Avoid public Wi-Fi or unsecured networks.

- Regular Software Updates:

- Apply security patches promptly to OS and wallet software.

5.2 Key Management Protocol

| Step | Instruction |

|---|---|

| 1 | Generate private keys on air-gapped hardware wallet or offline device. |

| 2 | Write seed phrases on physical media (steel plate preferred, see Volume VIII: The Water Codex). |

| 3 | Store backups in geographically and jurisdictionally diverse secure locations. |

| 4 | Use multisignature wallets with threshold signing to distribute risk. |

| 5 | Rotate keys periodically or upon suspicion of compromise. |

5.3 Transaction Privacy Protocol

- Use coin mixing services or CoinJoin protocols (e.g., Wasabi Wallet) to obfuscate Bitcoin transaction trails.

- For privacy coins, enable default privacy features and avoid address reuse.

- Route transactions through privacy networks (Tor) to prevent IP linkage.

- Use VPNs with no-logs policies.

5.4 Threat Modeling and Response

| Threat Vector | Detection Method | Response Action |

|---|---|---|

| Phishing Attacks | Suspicious communications | Verify URLs manually; never disclose keys |

| Malware Infection | Regular antivirus scans; system monitoring | Isolate device; wipe and restore from backup |

| Physical Theft | Secure physical storage (safe, vault) | Enable hardware wallet PINs; destroy compromised seeds |

| Network Surveillance | Traffic analysis tools | Switch VPNs; use Tor; change network behavior |

Section 6: Integrated Use Cases and Risk Assessments

6.1 Use Case: Micro-payments with Lightning Network and Privacy Coins

- User A opens LN channel funded with Bitcoin.

- User A sends payment to User B via LN.

- User B converts received Bitcoin to Monero using atomic swap protocol.

- User B spends Monero for private purchase.

Risk Assessment:

| Risk | Severity | Mitigation |

|---|---|---|

| Channel Closure Fraud | High | Use watchtowers; monitor channels |

| Atomic Swap Failure | Medium | Use trusted swap protocols |

| Network De-anonymization | Medium | Use Tor and VPNs |

| Liquidity Limitations | Low | Maintain multiple channels |

6.2 Use Case: Yield Farming with DeFi and Smart Contracts

- User deposits stablecoins into a DeFi yield aggregator.

- Aggregator smart contract allocates funds to multiple protocols.

- Interest and rewards accrue, distributed to user.

- User withdraws funds and rewards.

Risk Assessment:

| Risk | Severity | Mitigation |

|---|---|---|

| Smart Contract Bugs | High | Use audited aggregators; diversify holdings |

| Governance Attack | Medium | Participate in governance; monitor proposals |

| Impermanent Loss | Medium | Understand underlying pools; reduce exposure |

| Regulatory Intervention | Medium | Use decentralized protocols; monitor compliance |

Conclusion

This volume imparts the profound knowledge essential for the modern financial practitioner: the Lightning Network’s scalpel for instant settlement, the cloaks of privacy coins, the dynamic altars of DeFi, and the autonomous logic of smart contracts. These tools, wielded with disciplined operational security, transform the user into an architect of economic sovereignty impervious to centralized control or surveillance.

Mastery demands exactitude, ceaseless vigilance, and a sacred commitment to the protocols herein. The path of the cryptoeconomic practitioner is fraught with peril and promise alike; this codex arms you with the shield and sword to prevail.

For further elaboration on cryptographic constructs and wallet architecture, consult Volume V: The Cryptographer’s Forge.

For exhaustive DeFi smart contract auditing techniques, see Volume IX: The Codebreaker’s Manuscript.

For detailed privacy network setup, refer to Volume VII: The Shadow Network Codex.

<!-- SECTION 6 -->

Volume III: The Physics of Sound Money

Chapter 3: Gold and Silver as Sound Money – Physical Properties, Historical Context, and Economic Roles

Introduction

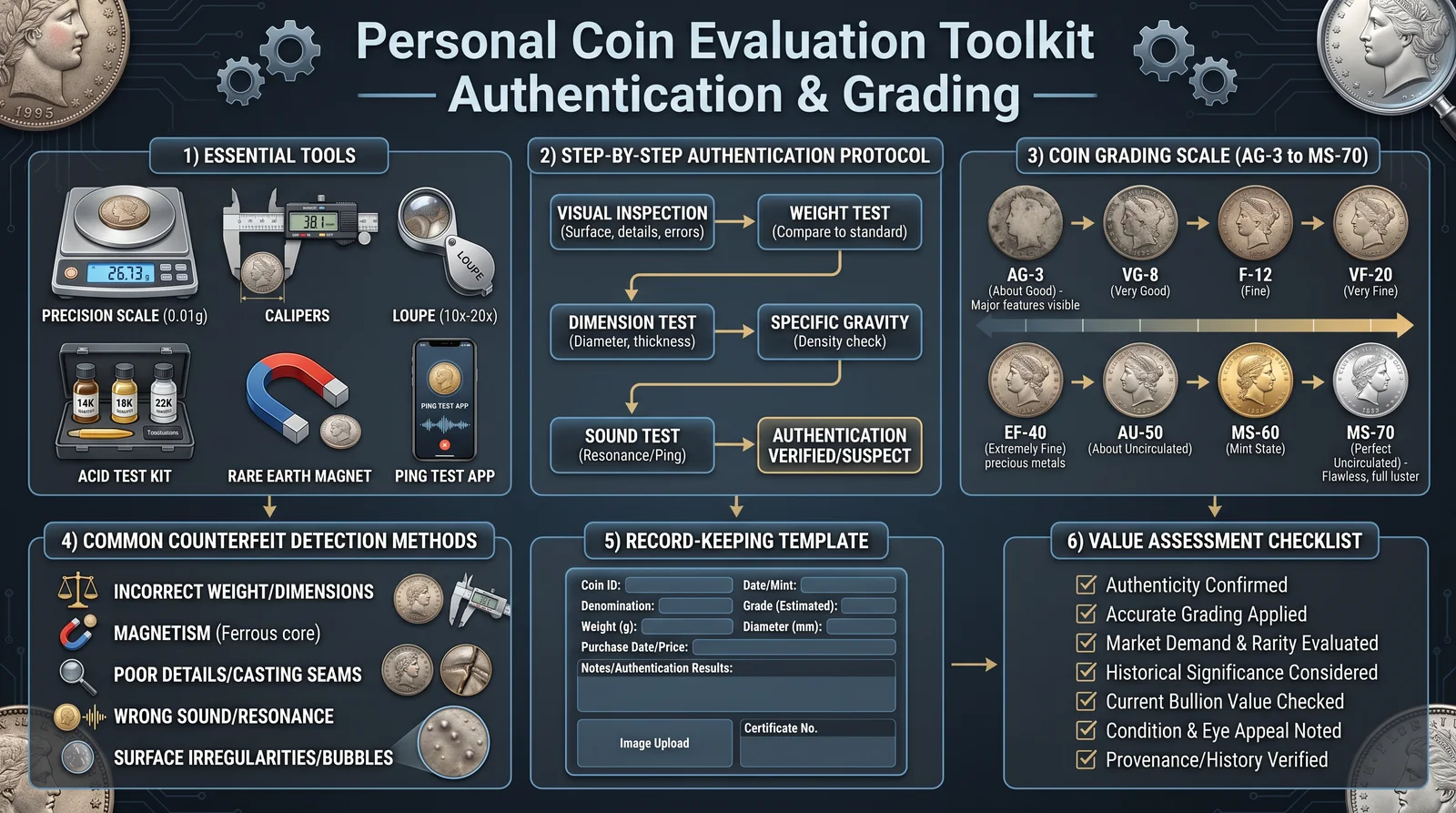

In the sacred pursuit of economic sovereignty and wealth building, the foundation lies in understanding sound money. Gold and silver, the twin pillars of monetary value for millennia, embody this principle through their unassailable physical properties and timeless economic roles. This chapter delivers a comprehensive treatise on these metals as sound money, culminating in Protocol 3.1.1 Acquisition and Verification, an exacting, stepwise procedure for authenticating bullion and coins.

I. The Physical Properties of Gold and Silver as Sound Money

The physical characteristics of gold and silver underpin their status as sound money. Their durability, divisibility, malleability, and scarcity are not incidental but intrinsic to their monetary function.

| Property | Gold (Au) | Silver (Ag) | Monetary Significance |

|---|---|---|---|

| Atomic Number | 79 | 47 | Determines chemical stability and density |

| Density (g/cm³) | 19.32 | 10.49 | High density resists wear; essential for weight-based verification |

| Melting Point (°C) | 1064 | 961.8 | High melting points resist counterfeiting by melting and recasting |

| Hardness (Mohs) | 2.5–3 | 2.5 | Softness allows minting detail; hardness sufficient to resist easy deformation |

| Malleability | Extremely malleable and ductile | Highly malleable | Allows precise coin striking and intricate designs |

| Corrosion Resistance | Excellent, non-reactive in air | Moderate, prone to tarnish | Gold resists oxidation preserving luster; silver tarnishes but does not corrode |

| Electrical Conductivity (MS/m) | 45.2 | 63.0 | Aids in advanced verification methods (electrical conductivity testing) |

Detailed Physical Analysis

- Density and Specific Gravity: Gold’s density of 19.32 g/cm³ is among the highest for naturally occurring metals. Silver’s 10.49 g/cm³, while nearly half gold’s, is still considerably dense relative to common metals. This density is the basis for specific gravity testing, a cornerstone verification technique covered in Protocol 3.1.1.

- Durability and Corrosion Resistance: Gold’s inertness protects it from tarnish or oxidation. Silver’s susceptibility to surface tarnish does not affect its intrinsic value but necessitates careful storage. Both metals maintain their physical integrity over centuries, enabling their use as long-term stores of value.

- Malleability and Minting: The softness and malleability of gold and silver allow for the intricate embossing and minting of coins, facilitating their role as standardized money. This physical adaptability is essential for the creation of mint-specific coinage with precise weight and dimension standards.

II. Historical Context of Gold and Silver as Sound Money

Historically, gold and silver have been the cornerstones of monetary systems since antiquity. Their universal acceptance, intrinsic value, and resistance to debasement preserved purchasing power across empires and centuries.

Key Historical Milestones

| Era | Event | Significance |

|---|---|---|

| 3000 BCE | Use of silver bars in Mesopotamia | Earliest recorded use of silver as trade medium |

| 600 BCE | Lydian electrum coins | First standardized coinage combining gold and silver |

| 50 BCE | Roman aureus and denarius | Established gold and silver coins as imperial currency |

| 1792 | US Coinage Act establishing gold/silver bimetallic standard | Formalized sound money in US currency system |

| 1870s | Gold Standard adoption globally | Fixed currency values to gold, stabilizing exchange rates |

| 1933 | US gold confiscation and end of gold standard | Marked shift to fiat currency; loss of sound money system |

| Present | Gold and silver as investment and reserve assets | Return to sound money principles in wealth preservation |

Economic Roles Over Time

- Medium of Exchange: Coins minted from gold and silver provided standardized units for trade.

- Store of Value: Their physical durability and scarcity preserved wealth across generations.

- Unit of Account: Monetary systems adopted gold and silver as benchmarks for currency valuation.

- Standard of Deferred Payment: Contracts and debts denominated in gold/silver coins ensured predictable value exchange.

Their scarcity and physical properties prevented arbitrary inflation and debasement, unlike fiat currencies. This chapter reveres these metals as sacred vessels of economic truth.

III. Economic Roles of Gold and Silver in Modern Sound Money

Despite fiat currency dominance, gold and silver retain critical economic functions:

- Wealth Preservation: Hedge against inflation and currency devaluation.

- Portfolio Diversification: Non-correlated asset reducing financial system risks.

- Monetary Anchoring: Central banks hold gold reserves to back national currency credibility.

- Industrial Demand: Silver’s unique physical properties create intrinsic industrial value, sustaining demand.

- Liquidity: Globally recognized, instantly tradable assets.

IV. Protocol 3.1.1: Acquisition and Verification of Gold and Silver Coins

The acquisition of physical gold and silver is the bedrock of economic sovereignty. Verification ensures authenticity, preventing loss through counterfeits or adulterated metals. This protocol outlines precise, actionable steps for verifying coins by weight, dimension, and specific gravity tests.

A. Equipment Required

| Item | Specification/Details | Purpose |

|---|---|---|

| Precision Digital Scale | Accuracy: ±0.01 g | Accurate mass measurement |

| Vernier Caliper or Micrometer | Accuracy: ±0.01 mm | Measuring diameter and thickness |

| Specific Gravity Test Kit | Includes: calibrated container, distilled water, and suspension apparatus | Density verification via water displacement |

| Magnet | Neodymium preferred | Detect magnetic alloys (gold and silver are non-magnetic) |

| Loupe or Magnifying Glass | 10x magnification minimum | Inspect coin detail and mint marks |

| Reference Mint Specifications | See Table 3.1.1 below | Compare measurements for authenticity |

B. Mint Specifications Table 3.1.1

| Coin Name | Metal | Purity (%) | Weight (g) | Diameter (mm) | Thickness (mm) | Mint Year Range | Notes |

|---|---|---|---|---|---|---|---|

| US Gold Eagle | Gold | 91.67 | 33.931 | 32.7 | 2.87 | 1986 - Present | 22K alloy, official bullion |

| Canadian Maple Leaf | Gold | 99.99 | 31.103 | 30.0 | 2.80 | 1979 - Present | Pure gold bullion |

| American Silver Eagle | Silver | 99.9 | 31.103 | 40.6 | 2.98 | 1986 - Present | Official silver bullion |

| Mexican Libertad | Silver | 99.9 | 31.103 | 40.0 | 3.15 | 1982 - Present | Uncirculated bullion |

| South African Krugerrand | Gold | 91.67 | 33.930 | 32.77 | 2.84 | 1967 - Present | 22K alloy, popular bullion |

C. Stepwise Verification Procedure

Step 1: Visual Inspection 1.1. Place the coin on a flat surface under a 10x loupe. 1.2. Observe the mint mark, year, and design details. Compare to known authentic specimens. 1.3. Check for signs of wear inconsistent with the coin’s age or suspicious surface anomalies.

Step 2: Weight Measurement 2.1. Zero the digital scale on a stable surface. 2.2. Place the coin gently on the scale. Record weight in grams to two decimal places. 2.3. Compare with official mint weight (Table 3.1.1). Acceptable variance: ±0.05 g.

| Weight Verification Outcome | Action |

|---|---|

| Within ±0.05 g | Proceed to next step |

| Outside ±0.05 g | Suspect counterfeit; reject or further analysis |

Step 3: Dimensional Analysis 3.1. Use vernier caliper to measure the diameter at coin center. Record in millimeters. 3.2. Measure thickness at multiple points, average measurements. 3.3. Compare measurements to mint standards (Table 3.1.1). Acceptable variance: ±0.1 mm diameter, ±0.05 mm thickness.

| Dimension Verification Outcome | Action |

|---|---|

| Within allowed variance | Proceed to next step |

| Outside allowed variance | Suspect counterfeit; reject or further analysis |

Step 4: Magnetic Test 4.1. Place neodymium magnet near the coin surface. 4.2. Observe any attraction or repulsion. 4.3. Gold and silver are non-magnetic; any magnetic response indicates counterfeit or alloyed metal.

| Magnetic Test Outcome | Action |

|---|---|

| No reaction | Proceed |

| Magnetic response | Reject coin as counterfeit |

Step 5: Specific Gravity Test

Specific gravity (SG) is the ratio of a substance’s density to that of water at 4 °C (1 g/cm³). For gold and silver, SG is a definitive authenticity test.

5.1. Fill a calibrated container with distilled water at room temperature (20°C recommended). 5.2. Zero the scale with the container filled. 5.3. Weigh the coin in air; record mass (m_air). 5.4. Suspend the coin fully submerged in water without touching container sides; record submerged weight (m_water). 5.5. Calculate SG using:

SG = m_air / (m_air - m_water)

5.6. Compare to known values: Gold = 19.32, Silver = 10.49. Acceptable variance ±0.1.

| Specific Gravity Verification Outcome | Action |

|---|---|

| Within ±0.1 of known SG | Coin verified authentic |

| Outside ±0.1 | Suspected counterfeit; reject |

D. Verification Checklist Table 3.1.2

| Verification Step | Measurement/Observation | Acceptable Range/Result | Outcome (Pass/Fail) | Notes |

|---|---|---|---|---|

| Visual Inspection | Mint mark, design, surface | Matches authentic coin | ||

| Weight Measurement | Weight in grams | ±0.05 g from mint specification | ||

| Diameter Measurement | Diameter in mm | ±0.1 mm from mint specification | ||

| Thickness Measurement | Thickness in mm | ±0.05 mm from mint specification | ||

| Magnetic Test | Reaction to magnet | No reaction | ||

| Specific Gravity Test | Calculated SG | ±0.1 from reference value |

V. Conclusion

Gold and silver’s exceptional physical properties, woven with their millennia-spanning historical roles, forge them as the immutable foundation of sound money. Mastery over their acquisition and verification, as codified in Protocol 3.1.1, is a sacred duty for the practitioner of economic sovereignty. Through rigorous adherence to these procedures, one safeguards wealth against deception and decay, preserving the eternal truth of monetary value.

Next Steps: For detailed metallurgical and assay techniques beyond physical verification, see Volume VIII: The Metallurgy Codex, Chapter IV: Advanced Precious Metal Assaying.

End of Chapter 3

<!-- SECTION 7 -->

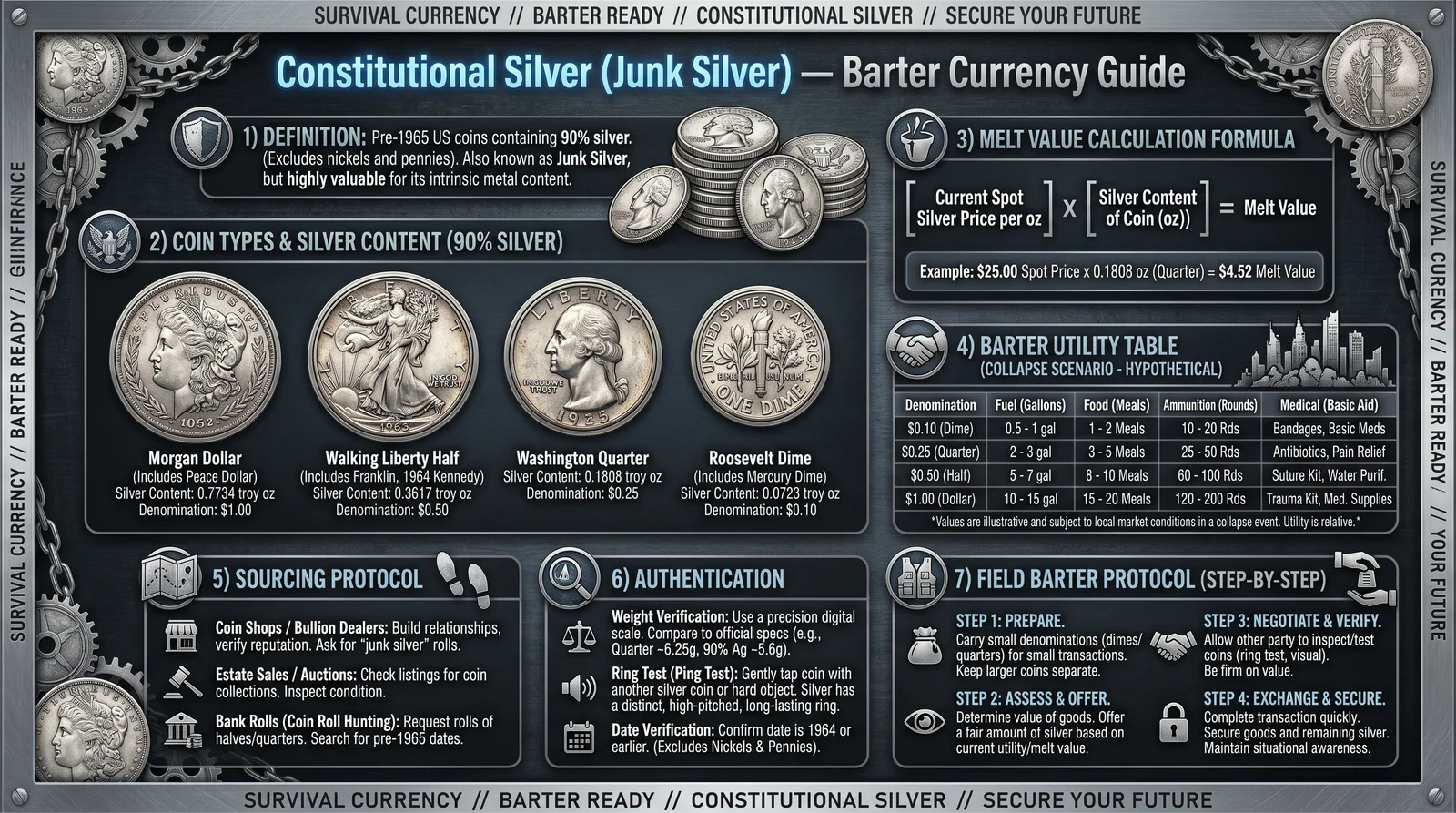

The Complete Practitioner's Codex, Volume 12

Chapter IV: Constitutional Silver (Junk Silver) — The Economist's Cipher for Barter and Liquidity

Introduction: The Sacred Metal of Economic Sovereignty

Within the sacred annals of economic mastery lies the true power of Constitutional Silver—pre-1965 United States silver coinage, hereafter known as Junk Silver. This metal, minted under the authority of the United States Constitution, carries intrinsic value far beyond its face denomination, embodying tangible wealth, immediate barter utility, and a hedge against fiat collapse. This chapter unveils the exact protocols, analytical frameworks, and acquisition strategies necessary to wield this financial tool with precision and sovereignty.

Section I: The Anatomy of Constitutional Silver — Definitions and Scope

Constitutional Silver (Junk Silver) refers exclusively to US coinage minted prior to 1965 wherein silver content is at least 90% by weight. These coins contain no numismatic premium in this context and are valued solely for their precious metal content and fractional barter utility.

Key Classes of Constitutional Silver Coins:

| Coin Type | Minting Years | Silver Purity | Typical Weight (g) | Silver Content (g) | Face Value (USD) |

|---|---|---|---|---|---|

| Half Dollar | 1948–1964 | 90% | 12.5 | 11.25 | 0.50 |

| Quarter | 1932–1964 | 90% | 6.25 | 5.625 | 0.25 |

| Dime | 1946–1964 | 90% | 2.5 | 2.25 | 0.10 |

| Half Dime | 1794–1873* | 90% | 1.35 | 1.215 | 0.05 |

*Half Dimes are rare and typically hold collector’s value beyond bullion content; excluded from most barter protocols.

Section II: Fractional Barter Utility – The Precision of Divisible Wealth

1. Fractional Value and Barter Efficiency

The genius of Constitutional Silver lies in its fractional denominations which allow for precise value exchange without reliance on fragile fiat systems or electronic records. Each coin's silver content aligns closely with its face value, allowing it to be used in barter scenarios as a trust-backed commodity.

Fractional bartering enables:

- Precise pricing of goods/services in increments as low as 10 cents worth of silver.

- Universal acceptance due to constitutional legitimacy.

- Portability and divisibility without the need for complex assay tools in the field.

2. Silver Content vs. Face Value

The following table details each denomination’s silver content and its approximate intrinsic value based on silver spot prices. This allows for direct conversion of market value to barter value.

| Coin Type | Silver Content (troy oz) | Face Value (USD) | Silver Spot Price per oz (USD) | Intrinsic Silver Value (USD) | % Over Face Value |

|---|---|---|---|---|---|

| Half Dollar | 0.3617 | 0.50 | 25.00 | 9.04 | 1708% |

| Quarter | 0.1808 | 0.25 | 25.00 | 4.52 | 1708% |

| Dime | 0.0723 | 0.10 | 25.00 | 1.81 | 1708% |

*Values are based on a $25/oz silver spot price. Intrinsic value scales linearly with spot price.

Section III: Complete Protocol for Sourcing Constitutional Silver

Step 1: Define Your Acquisition Objectives

- Determine target volume: e.g., 10 oz, 50 oz, or 100 oz of silver.

- Define denominations based on barter needs (half dollars preferred for bulk, dimes and quarters for fractional exchanges).

Step 2: Identify Reliable Acquisition Channels

- Local Coin Dealers: Preferred for physical inspection and immediate verification.

- Online Bullion Marketplaces: Use only verified vendors with strong escrow or buyer protection.

- Estate Sales and Auctions: Potential for discounted bulk acquisition.

- Secondary Barter Networks: Established treasure circles and barter groups.

Step 3: Verification Protocols for Authenticity

- Visual Inspection:

- Confirm minting date is pre-1965.

- Check for wear consistent with circulation; counterfeit coins often show inconsistent wear or tooling marks.

- Weight Measurement:

- Use a calibrated digital scale with ±0.01 g accuracy.

- Half dollar expected: 12.5 g ± 0.1 g.

- Quarter expected: 6.25 g ± 0.05 g.

- Dime expected: 2.5 g ± 0.02 g.

- Magnet Test:

- Constitutional silver is non-magnetic.

- Any magnetic attraction indicates base metal counterfeit.

- Ring Test (Optional for Advanced Users):

- Tap the coin gently on a hard surface; authentic silver rings with a distinct, sustained tone.

- Counterfeits produce dull or short tones.

- Acid Test (Destructive, Last Resort):

- Use a silver testing acid kit.

- Apply a drop of acid on a small scratch or edge; silver will exhibit a specific color reaction.

- XRF Analyzer (Advanced, Non-Destructive):

- Use if available for precise compositional verification.

Step 4: Secure Storage Post-Acquisition

- Store coins in airtight, inert containers (e.g., silicone-sealed plastic flips) to prevent tarnish.

- Maintain a ledger with serial numbers, acquisition dates, and verification notes.

- For bulk storage, use vault-grade security with temperature and humidity control.

Section IV: Barter Utility and Valuation in Field Operations

1. Valuation Table for Barter Negotiations

| Coin Type | Silver Content (grams) | Approximate Market Value (USD) | Typical Barter Equivalent | Notes |

|---|---|---|---|---|

| Half Dollar | 11.25 | 9.04 | 1 lb of flour, 1 gallon fuel equivalent | Preferred for large value exchanges |

| Quarter | 5.625 | 4.52 | 0.5 lb sugar, 0.5 gallon water equivalent | Good for medium transactions |

| Dime | 2.25 | 1.81 | Small goods, cigarettes, minor repairs | Ideal for small transactions |

*Values fluctuate with silver spot price; adjust barter equivalents accordingly.

2. Fractional Barter Techniques

- Utilize coin combinations to approximate exact barter amounts.

- For example, a barter value of $15.00 can be met with 1 half dollar (9.04 USD) + 2 quarters (9.04 + 9.04 = 18.08 USD) minus agreed discount for overpayment.